Daniel Waldenstrom makes the case at Foreign Affairs The Inequality Myth. Excerpts in italics with my bolds and added images.

Western Societies Are Growing More Equal, Not Less

Spend a few minutes browsing political commentary or scrolling social media and you will discover a seemingly settled truth: inequality in the West is soaring, the middle class is being hollowed out, and democracies stand on the brink of oligarchy. The idea is seductive because it fits everyday anxieties in many Western countries—housing has grown increasingly unaffordable, billionaire wealth mushrooms unfathomably, and the pandemic exposed yawning gaps in social safety nets. Yet the most influential claims about inequality rest on selective readings of history and partial measurements of living standards. When the full balance sheet of modern economies is tallied—including taxes, transfers, pension entitlements, homeownership, and the fact that people move through income brackets across their lives—the story looks markedly different. Western societies are not nearly as unequal as many believe them to be.

Getting the facts right matters because bad diagnosis breeds bad prescriptions. If governments assume that capitalism is inexorably recreating the disparities of the Gilded Age, they will reach for wealth confiscations, price controls, or ever-larger public sectors funded by fragile tax bases. If, instead, the evidence shows that free-market economies have enriched middle classes by expanding asset ownership, that entrepreneurs’ fortunes are associated with advances shared with the broader public, and that much of the post-1980 rise in recorded inequality reflects methodological quirks, then a different agenda follows: states should encourage ambition, protect competition, widen access to wealth-building, and ensure that public services complement—not smother—private prosperity.

In short, before treating inequality as an existential crisis,

it is worth double-checking the thermometer.

Conventional Wisdom Overturned by Evidence

The canonical data tell only part of the story, and the least flattering part at that. A growing body of scholarship reassesses the long-run distribution of wealth by adding what earlier studies neglected. Three findings stand out.

First, private wealth has exploded—but so has broad ownership of it.

Reconstructed national balance sheets for France, Germany, Spain, Sweden, the United Kingdom, and the United States show real per-adult wealth roughly tripling since 1980 and rising more than sevenfold since 1950. Crucially, an increasing share of that capital sits in the homes and pension funds of ordinary households. In 1900, assets held by the elite—agricultural domains and shares in industrial or financial corporations—dominated; today, residential property and funded retirement accounts represent the majority of private assets. That shift parallels mass homeownership: in most Western countries, 60 to 70 percent of households now own the roof over their heads—an equity stake unavailable to their great-grandparents. Most workers hold pension claims in mutual funds or index funds, granting them the high returns of stock markets at low risk—what amounts to financial democratization.

Second, wealth concentration has fallen—not risen—over the past century.

In Europe, the top one percent now owns barely a third of the share it held in 1910, right before the beginning of the transformative era of world wars, democratization, and the growth of governmental capacity, and since the 1970s that share has been essentially flat, even as real wealth—that is, wealth adjusted for inflation—has tripled with rising asset prices. The United States shows a clearer uptick beginning in the 1970s, most visible among the spectacular fortunes of tech and finance titans, whose gains have outpaced even the impressive wealth growth of the middle class. Yet U.S. concentration remains closer to its 1960 level than to its pre-1914 peak.

The dominant quantitative fact of the century, therefore,

is not a new Gilded Age but a dramatic wealth equalization

propelled by mass asset ownership.

Third, the fact that people move through different income brackets over the course of their lives should temper typical measures of inequality.

So, too, should the effects of welfare payments. Annual snapshots lump graduate students with retirees living off savings, making income and wealth gaps appear wider than lifetime consumption gaps. When studies in different countries instead follow individuals over time, they typically find that within only a few years, half the households in the bottom income decile have climbed to higher levels. Many top-decile households can drop to lower rungs of the ladder after business or investment setbacks. Government welfare programs further compress differences. In Sweden, when public pension entitlements are capitalized and added to assessments of personal wealth, this alone cuts the measured wealth inequality—known as the Gini coefficient—by almost half. In the United States, the market’s redistributive role is smaller, but when Social Security, Medicare, and employer-provided health insurance are treated as in-kind income, median households fare far better than raw wage data suggest.

Social Alarmists Out of Touch with Today’s Realities

These facts undermine the image of an inexorably widening chasm between a plutocratic elite and the rest. Yes, superstar entrepreneurs have amassed fortunes measured in tens of billions. But that outcome signals success, not failure: they furnished goods and services that millions freely bought. Their booming companies also supply jobs, higher wage earnings, and substantial tax revenue—directly through profits and payrolls and indirectly by raising the broader tax base. Over the past four decades, life expectancy in advanced economies (including in the United States despite the much-noted increase in “deaths of despair”) rose roughly six years, high school completion became nearly universal, and personal computers once reserved for elites went mainstream.

Those who typically bemoan the rise of inequality

don’t correctly weigh the size and division of the pie.

Rising real incomes and higher asset values are preconditions for mass prosperity and for a well-funded public sector. Even advocates of government intervention should champion efficient growth: every percentage point of GDP adds billions to tax revenue. The West’s most durable path to fairness, then, is to scale up the channels through which ordinary households acquire assets—including affordable housing supply, portable retirement accounts, and low-fee index funds—and to keep markets open so new firms can challenge incumbents.

That perspective should also moderate calls for annual taxes on the stock of net wealth, which have recently been proposed by some politicians and researchers, and have even been discussed officially at G-20 and UN meetings. These so-called wealth taxes are problematic because they hit illiquid assets, forcing entrepreneurs or farmers to borrow or liquidate. Scandinavian experience of such taxes shows that they produce meager revenues, come with high administrative costs, and encourage capital flight. If capital is to be taxed, a more efficient and equitable way is to tax capital income—such as dividends, realized gains, and corporate profits.

Evidence-based Priorities for Policymakers

Misreading inequality courts several risks. It diverts energy from the real challenges to Western economies, which include lax productivity growth, aging populations, and the imperatives of climate adaptation. These problems will strain public budgets. But excessive state-centrism and confiscatory wealth taxes impede capital formation and make financing those tasks harder, not easier. Misunderstanding inequality also breeds regressivity: taxing housing wealth indiscriminately can hit asset-rich but cash-poor retirees; taxing private firms can force sales to multinational giants with cheaper credit. And it corrodes trust: when citizens hear that capitalism benefits only the elite—even as their own living standards rise—they may grow cynical about official statistics and susceptible to populist cures worse than the disease.

A more accurate reading of the data supports a balanced agenda. To be clear, excessive wealth concentration poses risks—most notably to political integrity. Transparent rules for campaign financing and party contributions are essential to minimize the undue influence of money. Core welfare services, such as education and health care, should not become overly dependent on private funding, otherwise they would tie the quality of care to personal wealth—and in the process deepen inequality. The solution is not to curb wealth itself but to safeguard the integrity of political institutions and ensure equitable access to public goods.

States should celebrate entrepreneurial success and foster competition by reducing regulatory burdens—especially those that disproportionately affect smaller and younger firms. Taxation on labor income should be modest enough to incentivize hard work and also allow for the accumulation of new wealth, while capital taxation should target income rather than wealth or inheritances. Public investment should focus on building the capabilities that let households become stakeholders—education, infrastructure, and a rules-based climate that rewards risk-taking. Such an agenda accepts that inequality can coexist with, and even flow from, broad prosperity. Frustration with privilege should be channeled into reforms that expand opportunity rather than cap success.

This agenda advances neither laissez-faire complacency nor egalitarian maximalism. It is an acknowledgment that the West’s most remarkable achievement is not the fortune of a Jeff Bezos or Bernard Arnault but the mundane riches enjoyed by millions whose grandparents lived without antibiotics, central heating, or college degrees. Policymakers would do well to remember that progress before they diagnose calamity—and nurture the conditions that make it possible: secure property rights, open markets, and an efficient public sector powered by the very economic growth its advocates sometimes disparage.

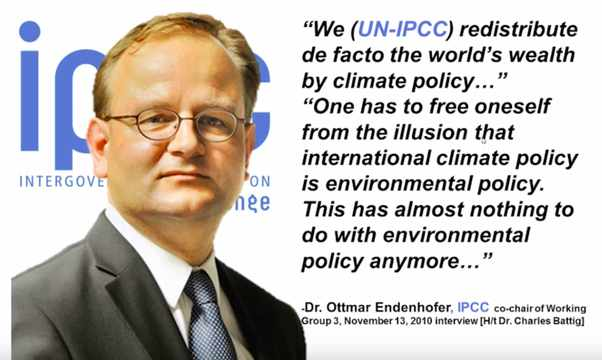

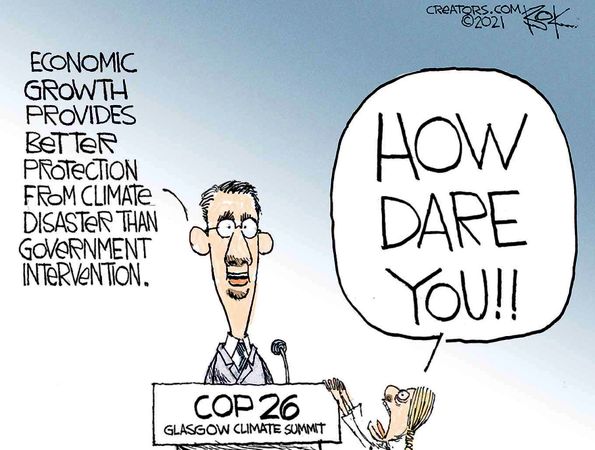

Footnote: The issue of adapting to climate change, raised in the article, perfectly illustrates the dichotomy of social perspectives regarding equality.

Ron, I greatly appreciate your blog and frequently forward it or post it to social media. However I have changed my email from jimchurch@telus.net to jimchurch91@gmail.com jimchurch91@gmail.com Please update my information so I continue getting your marvellous missive. Jim Church

LikeLike

Jim, thanks for attending my blog. I deleted your old address and added your new one. Let me know if that works.

LikeLike