BREAKING: U.S. Unleashes $10 Billion Nuclear Shockwave To Revive Belgium’s Energy!

Mackenzie Web reports on an announcement in Belgian news site La Libre “The United States wants to help Belgium restart its nuclear power plants, Donald Trump is fully behind the project” (translation) Excerpts in italics with my bolds and added images.

In a bold revelation, U.S. Ambassador to Belgium Bill White announced a game-changing investment plan that shifts the energy landscape of Europe. America is prepared to finance up to 50 percent of new nuclear reactor construction in Belgium, potentially injecting $10 billion into this initiative. His remarks, delivered to the Belgian newspaper La Libre, signal a renewed focus on nuclear energy as a reliable power source. White, clearly aligned with Trump’s energy strategy, stated,

“Washington is all-in on helping Belgium reverse decades of suicidal green phase-out madness.”

Several MEPs (mainly Greens) hold up anti-nuclear posters at EU debate.

This renewed commitment comes at a pivotal time for Belgium as it seeks to reclaim its energy independence. The country’s new right-leaning government, led by Prime Minister Bart De Wever, is actively nationalizing its nuclear fleet and abandoning plans to decommission existing reactors. No longer willing to rely on inconsistent renewable energy sources, Belgium is stepping back into its nuclear past, which had been shunned during years of leftist climate policies prioritizing wind and solar over proven energy sources. As White puts it, the reality of energy security is finally sinking in.

American companies Westinghouse and GE Vernova are set to lead the charge in this nuclear renaissance. Westinghouse’s AP1000 reactor, equipped with advanced passive safety features, promises a safer, more efficient alternative to outdated technologies previously favored in Europe. With an impressive capability for 72 hours of blackout protection, this reactor is already in operation in the U.S. and China, demonstrating its reliability. Similarly, GE Vernova’s BWRX-300 small modular reactor boasts rapid deployment capabilities, making it a perfect fit for Belgium’s urgent energy needs.

BWRX-300 Small Modular Reactor | GE Vernova Hitachi

The significance of this investment stretches beyond economics; it also reinforces America’s longstanding alliance with Belgium. White highlighted that this initiative harkens back to an 80-year partnership where the Belgian Congo’s uranium was pivotal in America’s atomic endeavors during World War II. The contribution of Belgian resources in winning past conflicts illustrates the strategic bonds between the two nations, and today’s nuclear cooperation continues that legacy. As White emphasizes, this is not merely a financial deal—it is a calculated move toward mutual security, ensuring that European nations can break away from fluctuating foreign energy supplies.

Moreover, this initiative marks a decisive pivot from recent energy decisions that left European nations vulnerable. The reliance on Russian and Middle Eastern sources has proven costly and unstable, especially amid geopolitical tensions. White asserts that under this new agreement, Belgium can expect “no more blackouts” and “no more skyrocketing bills,” fundamentally changing the energy conversation in Europe. With the U.S. stepping up to fill this critical void, the interests of American energy innovation directly align with the needs of a nation seeking stability.

In summation, this announcement is a shot across the bow to proponents of renewable energy who have long championed policies ignoring the realities of energy demand and practicality. The message is clear: America is not just offering financial assistance; it is providing a framework for a robust nuclear future. While globalists may resist this trend, the power of American engineering and technology is poised to reshape Belgium’s energy landscape, ensuring real leadership is showcased on the world stage. The green dream is receding, while the nuclear renaissance emerges, casting doubt on the feasibility of relying solely on renewables.

Zeldin explains how EPA grants cycled through multiple groups,

each taking a cut, before funding more activist groups.

Environmental Protection Agency (EPA) Administrator Lee Zeldin revealed how federal dollars spent on “environmental justice” often perpetuate a wasteful yet lucrative cycle of environmental activism. [some emphasis, links added]

“It’s the principle that there needs to be a zero tolerance policy for any waste and abuse,” Zeldin told host Alex Marlow. “It’s also the principle of being able to do more with less, and we proved over the course of our first 15 months here that we can achieve extraordinary savings here at the agency.”

EPA’s annual operating budget at the time of Zeldin’s arrival was “about $10 billion,” yet he said, “Over the first year that I was in this position, we saved $30 billion.”

“In 2024, this agency obligated and spent over $60 billion, and we were able to cancel grants and contracts. We did real estate consolidation [and] staff efficiencies with an agency-wide reorganization,” he explained. “We closed an EPA museum that nobody knew about or almost no one even visited.”

Zeldin pointed to an exchange with Senator Sheldon Whitehouse (D-RI) in a congressional hearing regarding wasteful solar grants that the self-proclaimed climate change champion supported.

“We had examples where the grant was going through up to four different pass-throughs, where each pass-through entity was getting at least 15% to administer their part of the pass-through,” Zeldin said. “I mean, a lot of this is just inexcusable.”

“The money that gets appropriated in the name of environmental justice to remediate an environmental issue, but then the dollar goes to an activist group to train other activist groups to come to D.C. and advocate for the next dollar to go to them to go out and be activists, like, wait, I thought we were spending this dollar to remediate an environmental issue,” he explained further.

“So yeah, it’s about doing more with less, and we have found extraordinary ways to save the taxpayers tens of billions of dollars.”

Tilak Doshi explains how formerly empirical economists have been captured by climatist ideology, betraying their profession and public trust. His Clintel article is UK economist says high energy prices are ‘good for the climate’. Excerpts in italics with my bolds and added images.

[Note: “In the old Soviet Union, the Communists allegedly used the term “useful idiot” to describe Westerners whose naïve political views furthered the Soviet agenda, even though these Westerners didn’t realize that they were being exploited in such fashion. It is in this context that I confidently declare that American economists have been useful idiots for the green socialists pushing extreme climate change policies.” Robert Murphy]

A UK economist recently said the quiet part out loud: high energy prices are ‘good for the climate’. This is not an aberration, says Tilak Doshi, but symptomatic of modern economists. “The barbarians did not storm the gates. The Western elites invited them in, gave them chairs, and asked them to redesign the curriculum.”

When petrol prices rocket because of supply shocks—such as the closure of the Strait of Hormuz and the rerouting of oil tankers—one might have expected a discussion of geopolitics, market signals and the obvious supply-side remedies. Of which there has been plenty, some competent and even masterly, some not so competent by “instant expert” talking heads in social and mass media. But a recent article by an economist in The Conversationoffered a solution so perversely tone-deaf it could have been lifted from a Babylon Bee satirical script.

Citing research that a 10 per cent rise in UK petrol prices can cut demand by up to 5 per cent, the piece solemnly declared that “high prices are a way of adjusting consumption to cope with the lower supply.” The subtext was unmistakable: with refined products suddenly scarcer, the proper response is not to produce more fuel if the country were blessed with domestic fossil fuel resources (like the UK) or to import more from sources outside the Strait of Hormuz or both. Instead, the advice from Christoph Siemroth, Senior Lecturer in Economics, University of Essex, is to make what little remains even costlier—so that the hoi polloi drive less, take the bus and hasten the glorious transition to net zero.

Clueless and Insidious

One is reminded of Marie Antoinette’s famous cake remark, betraying aristocratic cluelessness. But The Conversation article is something far more insidious: the capture of economics itself by the green ideology that now rules our institutions from the BBC to the Treasury, from Oxbridge common rooms to the UK Met Office service. The discipline that once stood as the last redoubt against the Frankfurt School’s long march through the social sciences has fallen. Frank Knight, Gary Becker, George Stigler, Milton Friedman et al held the gates against postmodern gibberish for a generation. No longer. The barbarians are inside the citadel, wearing lanyards from the oxymoronically named Department for Energy Security and Net Zero, chanting “sustainability” like a secular rosary.

Consider the elementary logic that every first-year economics student once absorbed before the PPE types at Oxford and Cambridge began their higher education in Gaia worship. When the price of a good rises because of scarcity—whether from a blockade in the Persian Gulf or an OPEC production cut—the signal is unambiguous: produce more, explore more, innovate more. Britain sits atop some of the richest hydrocarbon resources in Europe. North Sea oil and gas reserves are not physically exhausted; they are made economic infeasible in the face of Miliband’s punitive tax rates.

Onshore shale, barely scratched after a decade of regulatory vandalism,

could transform our energy security if the

“precautionary principle” were not treated as holy writ.

Higher prices should, in any sane world, trigger precisely that response: more drilling, more fracking, more investment in refining capacity, more imports of oil and gas from diversified suppliers. Instead, our green economists prescribe the economic equivalent of putting a feverish patient into a sauna. Demand must fall. Prices must stay punishingly high. The suffering is the point.

Taxes

The Conversation piece is exemplary in its genre. Price caps are correctly dismissed as distortionary, leading to physical shortages and queues as a means of rationing. One needs to only remember the long lines at gas stations in the US under Jimmy Carter’s price controls after the 1979 oil price shock.

Roughly 50–55% of the UK retail price for both petrol and diesel currently go to the government as taxes.But fuel duty cuts are rejected because they are untargeted and cost the Exchequer revenue—fuel duty, after all, is nearly 2 per cent of government income, a nice little earner for the net-zero industrial complex.

The preferred remedy? One-off cash transfers to low-income car owners, modelled on Germany’s 2022 gas rebate which provided a temporary fuel tax cut in 2022 to ease soaring petrol and diesel prices during the energy crisis triggered by Russia’s invasion of Ukraine.

The beauty of this, we are told, is that it preserves the “price signal” while letting households “profit” by leaving the car at home. Translation: we will bribe you to stay poor and immobile, all in the name of the planet. Meanwhile, the authors of such wisdom never feel the pinch. They lecture the white van plumber, carpenter or electrician going about his work and the hard-pressed mother doing the school run that their higher fuel bills are a feature, not a bug.

Luxury Beliefs and Intellectual Corruption

These are luxury belief-inspired energy policies which “confer status on the upper class at very little cost, while often inflicting costs on the lower classes”. As Victor Davis Hanson has so often pointed out, leftist policy elites in Democrat-run states suffer little from the consequences of their own policies. The metropolitan elite’s enthusiasm for open borders stops abruptly at the high walls of their own villas (Nancy Pelosi anyone?)

The same applies to energy. Inhabitants of the liberal metropolitan bubble can afford the £12-an-hour parking in Covent Garden, the retrofitted Victorian terrace with an air-source heat pump the size of a small car, and the Tesla whose real environmental cost is buried in Chinese lithium lakes and in artisanal cobalt mines using Congolese child workers. For them, “sustainability” is a lifestyle brand. For the rest of the country—pensioners choosing between heating and eating, hauliers facing bankruptcy, farmers unable to run their tractors—it is economic sadism dressed up as virtue.

Buddhist economist

The historical parallel is instructive. E.F. Schumacher — the “Buddhist economist” — told us, “small is beautiful” and that giant power stations were somehow spiritually corrosive. One wonders what he would make of the fact that a modern combined-cycle gas plant needs to be at least 200 MW to be remotely efficient, or that industrial civilisation runs on economies of scale, not backyard steel furnaces.

Yet today’s green establishment is repeating the Maoist folly in Western drag: decentralised “community energy”, intermittent wind and solar that require massive subsidies and backup gas plants, and an ideological insistence that the optimal size of an economy is whatever fits the carbon budget decreed by “climate modellers” in Exeter or East Anglia. The Soviet Union tried to create the New Soviet Man—selfless, collective-minded, liberated from base material desires. The project failed spectacularly. Its successor is the New Green Man, who measures his carbon footprint, cycles to the vegan restaurant, and cheers when Ed Miliband shuts down another North Sea field. The totalitarian impulse remains; only the Orwellian vocabulary has changed from “proletarian internationalism” to “just transition” and “climate justice”.

The intellectual corruption runs deep. Paul Krugman, a Nobel laureate in trade theory, now produces columns that read like press releases from the Church of Climate. Marginal costs of natural gas? Not so relevant when policy costs—carbon taxes, renewable obligations, network charges, capacity market payments—make up some 60% of your bill. As Kathryn Porter,David Turver and others have documented with forensic clarity, the “energy price crisis” is largely a net-zero policy-induced crisis. The wholesale cost of electricity is only part of the story; the rest is the deliberate layering of green levies and taxes that no classical economist would recognise as market-based. Yet we are told, with straight faces, that the “97 per cent consensus” demands we accept this as settled science. The same consensus, one notes, that once assured us the pause in global temperature increase was impossible, that polar bears were doomed, and that Himalayan glaciers would vanish by 2035.

Tyranny

Rupert Darwall’s Green Tyranny provides an insightful exploration into the origins of the climate industrial complex. The green movement’s roots lie not in empirical ecology but in a Malthusian revulsion against industrial modernity and a quasi-religious yearning for control. What to eat (less meat), how far to travel (fewer flights), what temperature your thermostat may reach (no more than 19°C if Whitehall has its way)—these are not technical questions but moral ones, policed by the new priesthood of economists who have traded the parsimony of Occam’s Razor for the abusive use of the precautionary principle (“better safe than sorry”). Uncertainty is weaponised asymmetrically so that minor or hypothetical risks (e.g., induced seismicity from fracking) trigger regulatory paralysis, while the far larger risks of alternatives are downplayed. The precautionary principle becomes a de-facto veto tool for ideological opposition to hydrocarbons, not genuine risk management.

Homo economicus, the rational maximiser embedded in cultural norms that Adam Smith understood in both The Wealth of Nations and The Theory of Moral Sentiments, has been replaced by Homo Climaticus: a creature whose every decision must be subordinated to the carbon ledger.

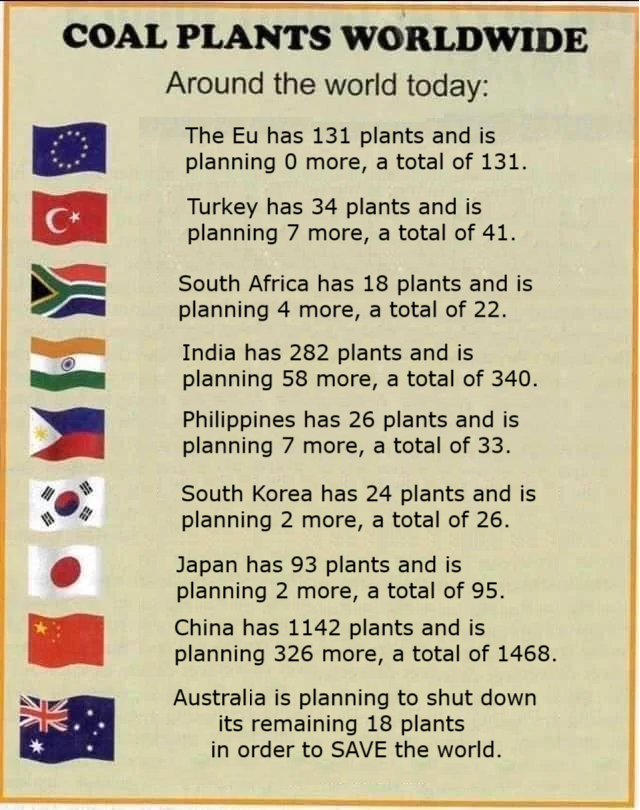

The consequences are not abstract. Britain’s energy prices are among the highest in the developed world precisely because we have chosen ideology over geology. While China adds coal-fired capacity equivalent to the entire UK grid every few years and India builds out its fossil infrastructure without apology, the West hectors the Global South about net zero and wonder why BRICS+ nations hedge their “policy commitments” to UN forums such as the COP30 conference in Brazil last year. The multipolar realignment is not just geopolitical; it is energetic. The Rest have noticed that the West’s net-zero experiment is self-inflicted economic suicide. They intend no such folly.

Glimmers of Hope or Barbarians At The Gates?

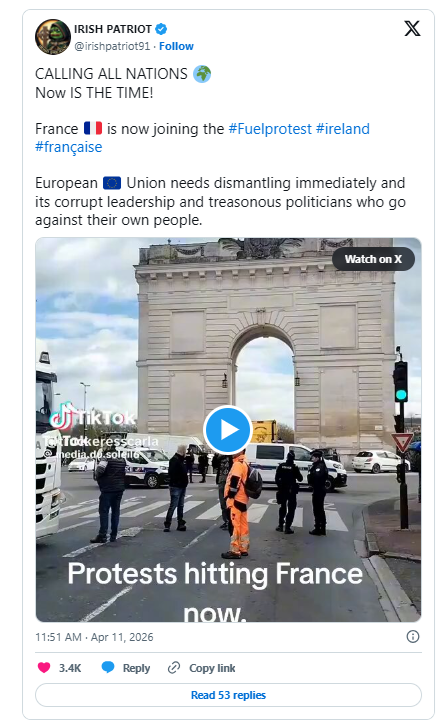

Yet there are glimmers of hope. The tide is turning, as Matt Ridley explains in his recent Clintel lecture “The Climate Parrot is almost dead.” Mr. Ridley argues that public and political momentum behind the “climate emergency” narrative is weakening. Indeed, public tolerance for green virtue-signalling has limits when the bills arrive. The on-going protests in Ireland over the cost of fuel by farmers, contractors and others have been massive, leading the government to place the army on “standby” as nationwide fuel protests continue to cause significant disruption and threaten critical supplies across the country. The military’s potential involvement comes as blockades outside major fuel depots intensify, prompting a dangerous government shift towards an “enforcement” phase in response to the escalating crisis. There are indications that these protests are spreading to Norway and France, as farmers and truckers there block arterial roads with tractors and trucks.

Populist movements across Europe and the United States are demanding energy realism: all-of-the-above policies that include nuclear, gas, and yes, even beautiful, black coal, where geology and economics dictate. The Chicago School may have been breached, but it is not yet razed. Rigorous economists—those still willing to follow the data rather than the grants—continue to point out that adaptation and technological progress have always outpaced apocalyptic forecasts. The “climate emergency” that justifies Soviet-style rationing by price is, on closer inspection, a political choice, not a scientific imperative.

Barbarians

Economics was once the most parsimonious of the social sciences, cutting through trite views with marginal analysis and revealed preference. When it abandons that discipline for the higher calling of Gaia worship, it ceases to be economics and becomes propaganda. The article in The Conversation is not an aberration; it is a symptom of a discipline that has exchanged truth for tenure and rigour for righteousness. The barbarians did not storm the gates. The Western elites invited them in, gave them chairs, and asked them to redesign the curriculum.

The corrective will not come from more white papers or behavioural nudges. It will come when voters—those whose lived experience of green policy is higher bills, colder homes, and slower journeys—demand an end to the experiment. Ireland is in tumult as we speak. Energy abundance is not a luxury; it is the foundation of modern civilisation. To pretend otherwise is not sophistication. It is civilisational self-harm. And the bill, as always, lands on the people least able to afford the eco-crucifix.

The above video includes a conversation between Bjorn Lomborg and Scott Bessent at the annual IIF gathering (Institute of International Finance). The introduction by IIF CEO Tim Adams starts about 11 minutes in. For those who prefer reading, below is a lightly edited transcript of comments back and forth, along with some added images. TA refers to Adams, BL to Lomborg and SB to Bessent.

TA: Today we’re going to deepen the discussion with a conversation between Bjorn Lomborg who runs the Copenhagen Consensus and the author how to spend 75 billion to make the world a better place. I’ve had this book on my desk since it was published in 2014. It’s a great publication. If you haven’t read it, you should. I’m sure Bjorn will give you some copies. It really is how do we do development and a cost benefit assessment? How do we get the most bang for our buck? And that conversation is often missed in this town and other capitals. And of course, we’re delighted and honored to have the Treasury Secretary Scott Bessent back today to join us at our spring meetings. So, ladies and gentlemen, please invite to the stage Bjorn and Secretary Scott Bessent.

BJ: Thank you very much. Tim, you kind of took away all our talking points. So, Mr. Secretary, it’s great to have a conversation here today about the World Bank and the IMF here at their spring meeting. The goals of these institutions, of course, is to accelerate global development, drive economic growth, and lift billions of people out of poverty. And these goals remain vitally important. Unfortunately, many development institutions now prioritize Western elite issues like gender, social topics, and climate change over what the world’s poorest people need and want: better education, healthcare, and reliable energy.

Nowhere is this disconnect more clear than in their climate fixation. In the latest year, 48% of the World Bank’s financing went to so-called climate finance, up from 44% the year before, exceeding their own uh 45% target. I suspect the reason why elites are so climate focused is because they correctly see the poor as more vulnerable to climate impacts. But remember, poor people are more vulnerable to every impact. They’re more vulnerable to disease, to hunger, to bad education, to corruption.

The World Bank and the IMF need to get back to making rational priorities. For instance, using cost benefit analysis. As Tim also just mentioned, these organizations used to lead the world in cost benefit analysis. As I’ve argued for a long time, and the reason I think we’re having this conversation now is that we need to scrap these climate targets and get the World Bank and IMF back to their core missions.

In your speech here last year at the IIF, you made this exact point and you called on the World Bank and the IMF to refocus on their core missions. In your view, how has the bank and the fund responded and what more do they need to do?

SB: Well, Bjorn, thank you and good good to be back here a year later to talk a little about a report card for the multilateral banks and to also say that the US leads the G20 this year and I can tell you that our agenda is growth. We believe in the US that the biggest risk to financial stability is a lack of growth.

When I look at the choices that Europe has made unable to follow the Draghy report from Mario Draghy on how to increase growth. The the EU was originally the European Economic Union and it was meant to facilitate trade among the members, make it more seamless, create more prosperity. And it turns out that it’s probably been a hint of the IMF and World Bank. I’m informed by Grace Hopper who was the first female Admiral in the US who was a big fan of it. She has some great sayings. Two of them, one is: The most dangerous words in the English language are “because we’ve always done it that way”. And the second is: “The way to get things done is to get things done.”

And I think we need to step back and look at the IMF and World Bank, their core missions. The IMF I believe the is global financial stability and stabilizing the countries that are in bad equilibriums and getting them back to a sustainable path an economically sustainable path. World Bank is to pull people out of poverty and we cannot have these kinds of elite beliefs get in the way. And I think a lot about this Nature magazine article that came out in April of 2024 that became the guiding principle for so much of the climate beliefs: that GDP was going to be 60% % lower by the turn of the century. So then it was the gospel for 18 months and then it was refuted.

So every everything was based on that. So you know I I don’t think that we can have this kind of short- termism. I think we have to stick with core principles and I do think we we are starting to see at at the World Bank. They are starting to take a tack more for energy abundance and all of the above. They have now gotten on board with nuclear energy. I’m not sure why it ever went away.

And then the IMF, I think, needs to lead by example, probably get rid of their golf course out in Maryland, which I said last year, and focus on global imbalances. Because I can tell you this slow motion buildup of global imbalances after a lack of sustainable growth, it is the the the biggest risk.

The the world cannot take a China with a trillion dollar trade surplus.

BL: And I think you’re absolutely right and one of those points that we we believe somehow that climate is so important that we need to do everything because the nature study that you mentioned that suggests that we could lose 60% of global GDP if we didn’t fix climate change. Which later turned out to be wrong, but of course the point is if that was really true, it should have been rich countries spending rich country money on dealing with climate change. But that’s not what’s happening. It’s mostly rich countries deciding to spend poor people’s money through the World Bank and the IMF badly. And this is not what the the world’s poor are telling us that they want.

So I I had the fortune to work together with Nobel laurate Tom Shelling and he often asked the very simple question, how do you best help poor people? Through development policy or through climate policy? Remember climate policy costs hundreds of trillions of dollars and it shaves off a tiny fraction of a degree in a century’s time. Development policy like avoiding death costs just billions or maybe even just millions of dollars and saves lives right now. And of course that is why development policy often is much much better if you actually want to help poor people.

And of course it also builds much more resilience. Look, a hurricane that hits poor Haiti kills hundreds of people. The same hurricane hitting rich Florida kills virtually no one because prosperity protects people. And so we need to get this conversation back and I think this is exactly where the IMF and the World Bank need to get back to their core missions.

SB: I think it has to be resiliency supply chains. Again, I think you know both the IMF and the World Bank have an important role in understanding this debt loop and downward spiral that many countries are in. Several countries, one in particular, have done the equivalent of a loan to own program. With a lot of these countries there’s a lot of undisclosed debt. There are a lot of tolling arrangements that are unfortunate and I think only the these multilateral banks can effectuate that.

But you know again I do want to congratulate them. The IMF was willing to say this time is different with Argentina and Argentina’s been a fantastic success. They’re accumulating reserves every day as we speak. Tens of millions of people there are being brought out of poverty. The government of Javier Milei, I’m very interested to see it was the poorest elements of Argentine society who voted for him this time around and the young people. So there there’s optimism there. And then you know that the IMF is working on bringing Venezuela back into making it look more like a normal economy, and I think will play a very important role there. And I think the World Bank leadership is back on a good trajectory in terms of energy and unlocking resources for the the very poorest countries.

BL: Yeah. If you don’t mind, I’ll pick you up on that energy point because last October you withdrew the United States from the Green Climate Fund. Because in your words, their goals run contrary to the fact that affordable, reliable energy is fundamental to economic growth and poverty reduction. I think that shows the general point we often forget, how energy really powers modern life. It warms us in the winter, it cools us in the summer, it transports us. I mean, look around this room and I think pretty much everyone is from somewhere else. And this is what energy does. Energy allows us to live better than kings of the past.

Energy really is prosperity. Yet, the climate fixation that we’ve been talking about means that both the World Bank and the IMF pushed for a rapid shift away from fossil fuels and towards renewables and for total ban fossil fuel investment. And I think they need a reality check. There is no transition that taking place globally. We use more renewables, yes, but we also use much more fossil fuels. The world still gets more than 80% of its total energy from fossil fuels. And the decline is so slow that on current trends, we will only get to 0% in 4 to 10 centuries.

Germany has spent famously 700 billion euros on its energy shift since 2002. Electricity prices more than doubled and yet Germany’s energy is still 79% fossil fuels. China produces most of the world’s solar panels, wind turbines and electric cars, but much of this of is produced with coal. China’s energy is still 87% fossil fuel. I would say a Chinese EV is a coal powered vehicle. Much of it is in China and of course especially in some places, for instance India, which are driven enormously on coal, they simply they emit more. But the real point is that poor countries want to get rich like China did. They want to use more energy and much of this will be fossil fuels. They don’t want to copy Germany and they don’t have 700 billion euros to blow on climate policies. So it is just simply hypocritical forcing poor nations into renewables that even rich Germany or China aren’t achieving.

In your IIF speech last year, you call on the World Bank to focus its efforts on expanding developing country access to reliable and affordable energy and you criticized its climate targets. You noted that the IMF devotes disproportionate time and resources on climate even though it’s not part of the fund’s mission. So, what have you seen from the bank and the fund in these areas since your speech? And what more do you expect from them?

SB: Again, as as I said earlier, I think the World Bank is has made a good pivot. They they are now pushing or they are a proponent of nuclear energy. I’m not sure how that wasn’t considered a renewable for for so many years. I mean, if if you look now, France is powering the European energy grid and their their reactors are running the full blast and it’s one of the cleanest. But when you think the Europeans got into this terrible recursive loop because they they decided to turn turn off their nuclear energy. The Germans became more dependent on Russian crude and then the Russians were selling them the crude to finance the war against them.

But you know I do think the World Bank is moving to an all of the above energy process and program and again is getting back to the core mission of lifting people out of poverty. And you know I would just say it’s very good to follow not only what people say but what they do. Bill Gates, who for a long time had pushed this climate agenda, has also changed tack. If you read his recent speeches he believes we’re going to innovate our way out of this. And the Gates Foundation has something like 13 billion of investment in energy innovation. Look no one’s expecting deos machina, one day and everything will be fixed. But in in the US we were going to run out of everything, going to run out of the crude and crude derivatives. And then fracking was invented and now that the the US larger reserves than Saudi and Venezuela.

On the other side, I think the IMF getting back to this message of stability, of monitoring global imbalances and stepping in early. You know I didn’t always agree with Ben Bernanke’s monetary policy, but I always admired Federal Reserve Chairman Bernanke because he had a framework. And if you ask him a question, you could almost see him run it through his framework and everything was always consistent. And I think with the IMF and the World Bank the framework needs to always be consistent.

BL: On the Bill Gates point I think really two things stand out. First of all, the innovation point that you just made. I mean this is what has always solved the problem. Tim mentioned the green revolution that we had in the 1970s when we worried about running out of food. Remember, we didn’t fix the problem of the world not having enough food by telling everyone, “I’m sorry. Do you mind not eating as much?” And then we’ll send it down to whoever it is that we worry about. The point was that we innovated a way to generate much more food.

And of course, we’ll do the same thing with climate. We are going to solve big problems through innovation. That’s how we’ve always done it. But I think Bill Gates made another point which is incredibly powerful and useful when you talk about climate change. He said: “For so long we’ve been talking about climate as if the point is to cut carbon emissions or to reach a certain temperature limit. No, the point is to make the world better for humans. And there the question is do we make the world better for humans by cutting carbon emissions by whatever tons? Or do we make it better by for instance making it so small children don’t die or that in school there’s so many other ways we can also do this or that. This of course refers back on the IMF and especially the World Bank on what can be done and there are just so many incredible things that we can do first.

SB: Yeah, again, you know, I think keeping focus on the main thing and not getting distracted by what feels good, it’s convenient, it’s part of the the Davos consensus while much of the Davos consensus seems to have been shattered.

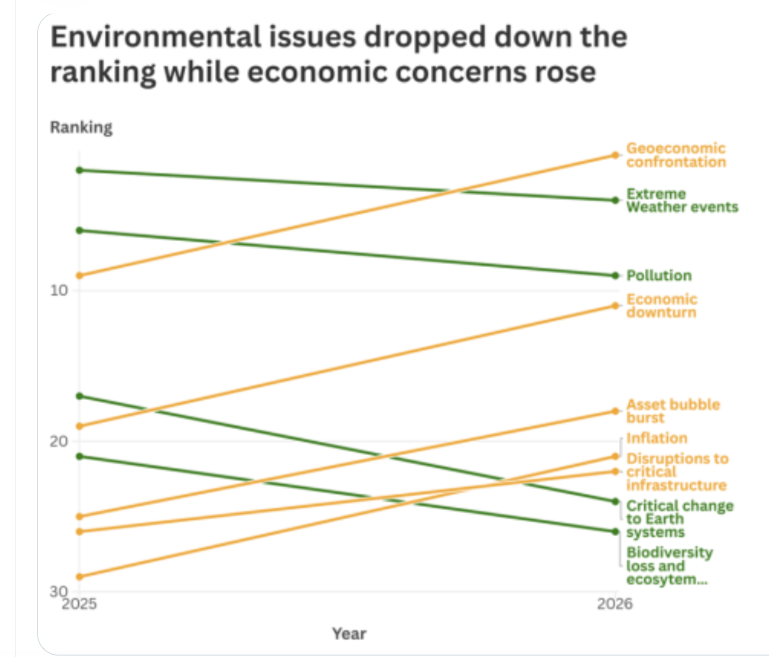

WEF’s Global Risks Perception Survey

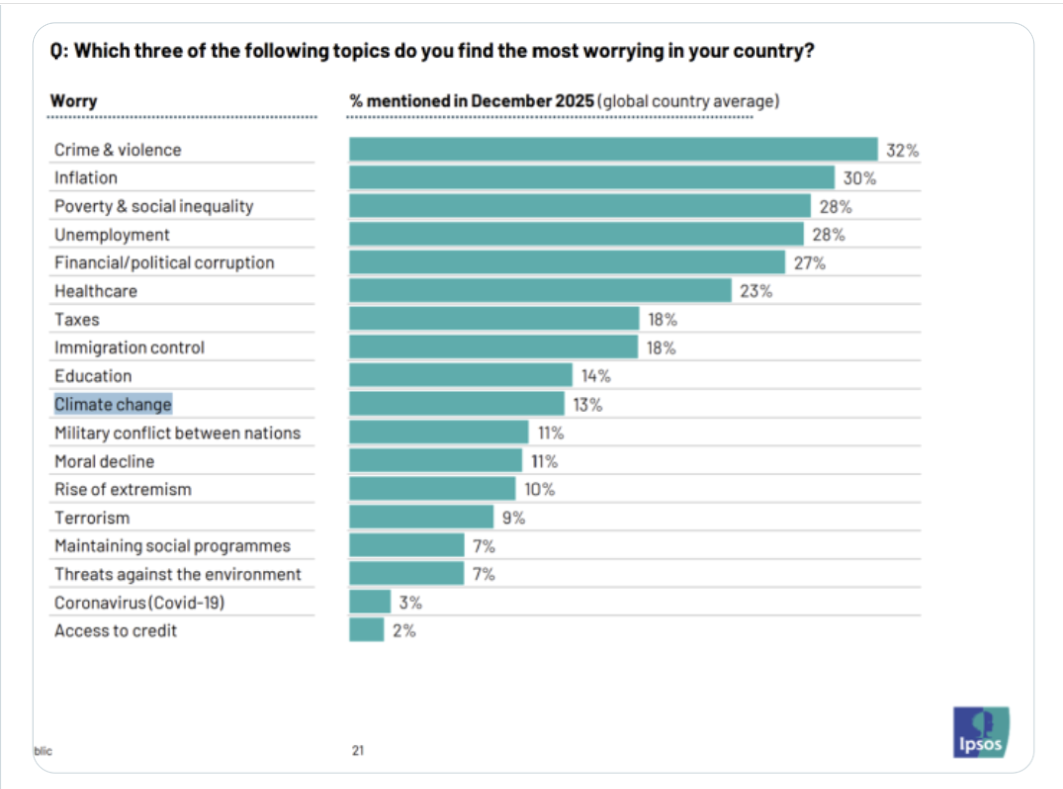

BL: Yes. So I want to just take us to our third and and and last point and talk about tradeoffs. Because all international financial institutions need to get back to the core point of tradeoffs. Look,the money that the World Bank spent on a solar panels can’t be invested in healthcare or education. And the world’s poor tell us very clearly not to focus on climate first. When Africans are asked what worries them the most, climate change came almost at the bottom. A vast survey of more than 50,000 Africans across 39 countries found that climate change ranked 31 of 34. The top concerns are not surprising there. It’s unemployment, the economy, health, education, poverty, roads, electricity, hunger, and corruption. And then it goes on for a long time until you get to 31, which is climate change.

When your child might die tonight from a preventable disease, no family cares about shaving a fraction of a degree off global temperatures in a century from now. Elected leaders of poor countries tell us the same thing. In a large survey of low and low middle- income countries, they show climate ranks 12 of 16 issues. Even the World Bank’s own client surveys show climate ranks low. So international financial institutions should compact to focus on their strengths. As you’ve said, the World Bank should focus on poverty reduction and the IMF on macroeconomic stability, but the world’s poor are very clearly saying don’t focus on climate first.

So from your perspective as treasury secretary, how do you view the international financial institutions and their effectiveness in general and the bank and the fund specifically?

SB: You know I would also highlight that it’s not a unique survey item among the world’s poorest. Germany instituted very very strict remodeling and rebuild requirements for German households. So you had to spend I can’t remember it was 30 40 50,000 euros to upgrade to a a more green house and they’re all getting voted out. So like probation is not a good motivator. I do think,as I said last year, that we are determined with the multilateral financial institutions the US wants to be in it to win it. We want to be good partners. America first does not mean America alone. And we we want to go back to basics.

These banks were invented around Breton Woods which was post World War II Europe and Asia, and was a unique time in America and it led to incredible prosperity the across the world. So, you know, why can’t we do that again? And why can’t we focus on growth? Like what are the tools? What what what is hindering growth of these economies? Is it the unsustainable debt which is is the IMF concern?

Is it the poor infrastructure, health and hygiene, which is the World Bank role?

Because you know for a time we kind of skipped the foundational elements and tried to jump to something else, kind of luxury beliefs, instead of issues when a government was not able to fund itself or if people were not able to feed themselves. We’ve just got to get back to that. I I think Ajay and Kristalina have have gotten the message and are moving forward in a very very constructive way and I want to congratulate them.

BL: When you have to decide what to do obviously I’m I’m an advocate for cost benefit analysis so I’m going to be saying they should be looking at it. Really, if you think about it, the World Bank and IMF used to be world leaders in cost benefit analysis. And it makes sense if you only have limited money. If you have to think about trade-offs all the time, you have to ask yourself where can we spend scarce resources and do the most good in the world. And this is exactly what cost benefit analysis does for you. It allows you to pick out the really good policies and make it just much more likely that we can actually achieve all these goals that we’re talking about.

A part of Battle of Ideas Festival 2025 was the above presentation explaining plainly why UK energy has become so expensive. For those who prefer reading, below is a transcript with my added bolds and images.

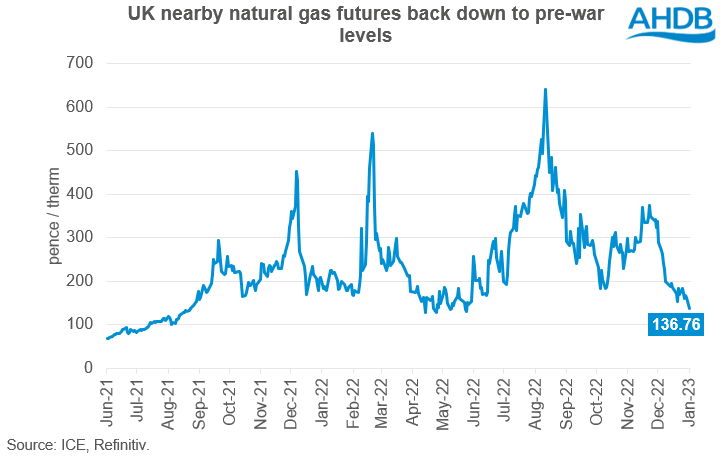

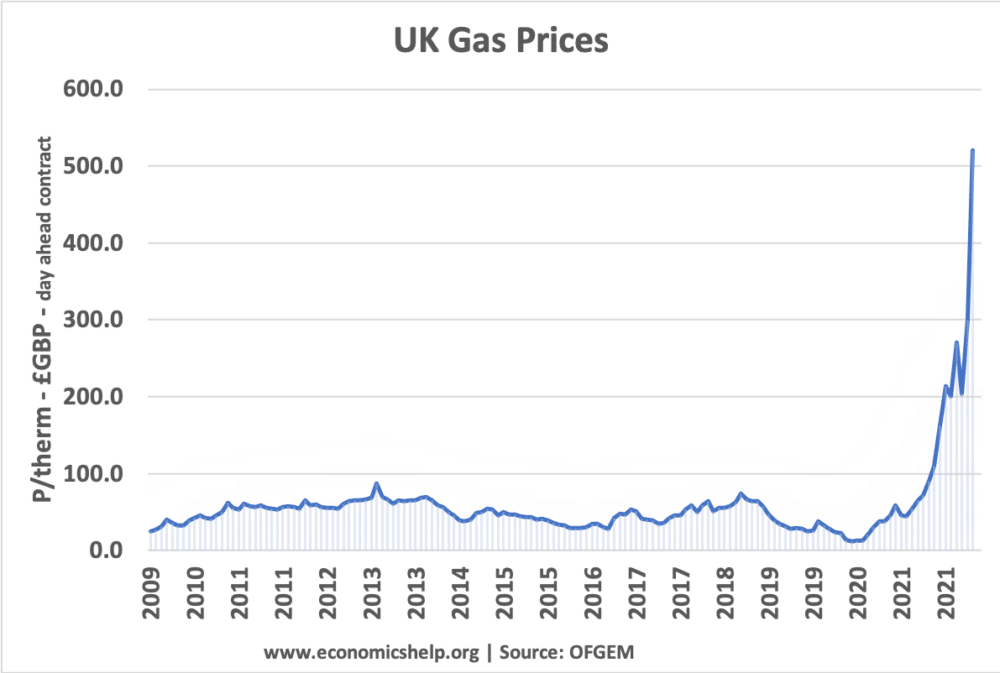

Why are our electricity bills so high? We’re told as Craig referenced that it’s all the fault of gas. Now this argument is going to come to somewhat crashing reality in the next year. I was just checking the prices now and from yesterday’s close we’re now87 percent down from the highs in 2022. Now has anybody seen an 87 percent reduction in their bills, hands up, anybody? Oh that’s a huge shock. Next year gas analysts expect that the gas price will return to its long-term average pre-2021.

So the gas crisis actually began in the autumn of 2021, about six months before the invasion of Ukraine and it was to do with the recovery from COVID. Basically during COVID demand for gas fell because industrial activity dropped, a lot of upstream production was shut in and it takes time to bring that back, you can’t just turn on the tap in most cases, it requires quite a bit more work than that. So there was a delay in bringing that production back online and when you have more demand than you’ve got supply then prices go up and then Putin took advantage of this in the following February and well we all know what happened then.

Since then in the upstream sector they’ve been busy bringing new LNG, liquefied natural gas projects, on stream. By the end of this year there’ll be enough new LNG to fully replace all of Russian gas and sometime next year we’re expecting the global gas market to go back into length. So there’ll be more supply globally than there is demand and prices are expected to fall. In fact the only reason why Miliband could possibly deliver the 300 pound reduction in bills would be because of gas prices falling.

Unfortunately I think he’s going to more than offset that with higher subsidy costs. So the first thing is that gas is not expensive and really for 25 years we had very low and very stable gas prices. Gas was cheap, in fact the cheapness of gas was what enabled the energy transition to even begin. I wrote a report earlier in the year about the cost of renewables, if you do a chart that shows the wholesale price of gas, the wholesale price of electricity and then the domestic price of electricity what you find is that the wholesale gas price was low and stable until 2021.

The wholesale electricity price was basically the wholesale gas price plus a little bit which is what you’d expect and then the domestic price was the wholesale price of electricity plus a little bit. And again you’d expect that you buy a wholesale, you pay for it to be delivered to your house, you’ve got to pay the supplier some money for you know doing the admin for that, they want to take a bit of profit, there’s some taxes, that’s what you’d expect.

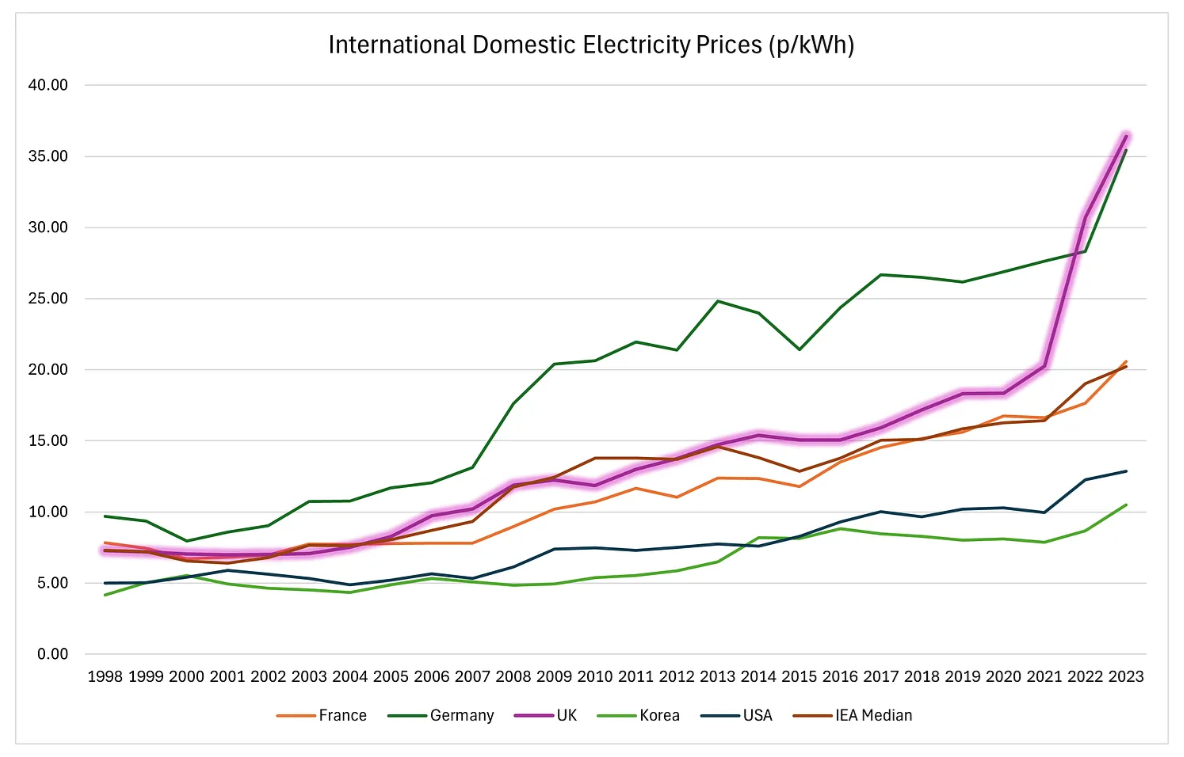

Figure 4 – International Domestic Electricity Prices (p per kWh). UK has the highest domestic electricity prices in the IEA.

But from 2006 this relationship started to break down and what we saw was a steep increase in what households were paying despite a flat trajectory for wholesale prices. Why was this? It was because we were adding on policy costs. We’re subsidizing renewables, we started using suppliers to do all sorts of other social programs, wealth redistribution, literally the warm homes discount is suppliers. They phone up the department for work and pensions and they find out which of their customers are eligible and then they calculate how much that discount is going to cost and then they add on an admin fee and then they spread that cost out across all our other customers.

They take money from one group of customers to give to another. This is wealth redistribution, it’s not the job of private companies. The energy company obligation, we’ve heard about that in the news this week where I think the National Audit Office has written a report saying how inefficient it is, how low quality the work is. Well guess what, energy companies are not experts in construction. They are being expected to engage in sub contracts to companies that will come in and install insulation and similar things in your home. They don’t know anything about this, this isn’t part of their core business.

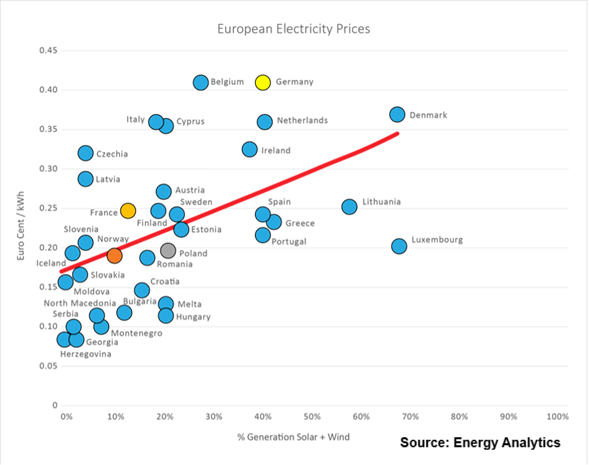

Typically as wind and solar power share of supply increases, distribution and transmission costs rise sharply.

It’s a hugely inefficient thing to expect suppliers to do and the cost of all that is added to bills. The smart meter rollout, we’re the only country in the world that expects suppliers, retailers, to install network equipment in people’s homes. Everyone else got the network companies to do it, you know, duh. And what’s even worse is that the supply business was created within the Utility Act 2000. It was the final part of unbundling the energy system and almost immediately both the governments and the regulators started telling everyone that suppliers were greedy profiteers that couldn’t be trusted.

And then they expressed shock that nobody wants these greedy profiteers who can’t be trusted to install devices in their home that would give the greedy suppliers that can’t be trusted lots of information about how they’re using electricity and gas and potentially enable them to change your prices remotely, put you onto prepayment tariffs remotely and do all sorts of other stuff remotely, potentially without your permission. And they were just kind of shocked that people didn’t want to do that. So the whole market is completely dysfunctional.

Now, when we come to the real costs and the real reasons that our bills are so high has to do with renewables. When we build renewable generation, we have to provide a big subsidy. Now, a lot of people think, well, the wind and the sun are free. And this is true. Wind energy and solar energy is free. But the equipment needed to turn that energy into electricity is not free. That’s actually pretty expensive.

Now, imagine that we only had renewables on our grid. And when you’re setting prices, normally, the price at which you sell your goods is linked to your short run marginal operating cost, which for wind and solar is close to zero. Essentially, you’d be giving it away. How are you going to recover your capital costs for that expensive equipment if you have to give away your products? You’re never going to be able to do it. So basic economic theory will tell you that renewables will never be built without subsidies. They are always going to require subsidies because you will never be able to recover the capital costs to selling the electricity at the short run marginal operating cost of that electricity.

So we give subsidies to renewables. And that subsidy is higher than the cost of generating electricity with gas. So the argument about gas pushing your bills up is nonsense. These subsidies are higher than the cost of generating electricity with gas. And the way the new subsidies work is that the generators are guaranteed a fixed price, and they receive that by selling that electricity in the market. And then if that’s lower than this fixed price, they get a top up.

And it’s a one for one relationship. If you lower the wholesale price of electricity by one pound, you increase the subsidy cost by one pound. And the subsidies are added to our bills. They come straight out of our pockets. So when people say, oh, we’ve got to get off gas, we’ve got to stop marginal pricing. People talk about marginal pricing as if we’re some weird outlier in the world markets doing this strange marginal pricing thing, taking the most expensive form of generation to set the price.

Every deregulated power market in the world sets the electricity price through marginal pricing. In fact, most commodity markets do the same thing. This isn’t weird. It’s completely normal.

And if you decided to change price formation to lower the wholesale price, your bill will stay the same. You’re just moving money in different buckets around the bill. Now the bit that says wholesale price will go down, and the bit that says policy costs will go up. But the amount you pay will stay the same. And so this is the whole misinformation that we have.

The other issues with renewables are you’ve got to pay for backup. They have low energy density, so you need a lot more wires to connect them. A good sized gas power station, 800 megawatts. If you wanted an equivalent size wind farm, you need 60 turbines. So that’s 60 times more wires. But to get the same amount of electricity over the year, because your wind is only working about a third of the time compared with about 86% of the time for gas, you need something like 150 times the wires. You need 150 turbines.

All that gets added onto your bills. The cost of backup to make sure you’ve got generation available when it’s not windy and sunny, that goes straight onto the bill. And the real-time balancing cost, where you’re having to even out the impact of clouds and gusts of wind, all goes on the bill. And so this is why our bills are so high.

The PM did abolish the consumer carbon tax,

though only by shifting it to businesses.

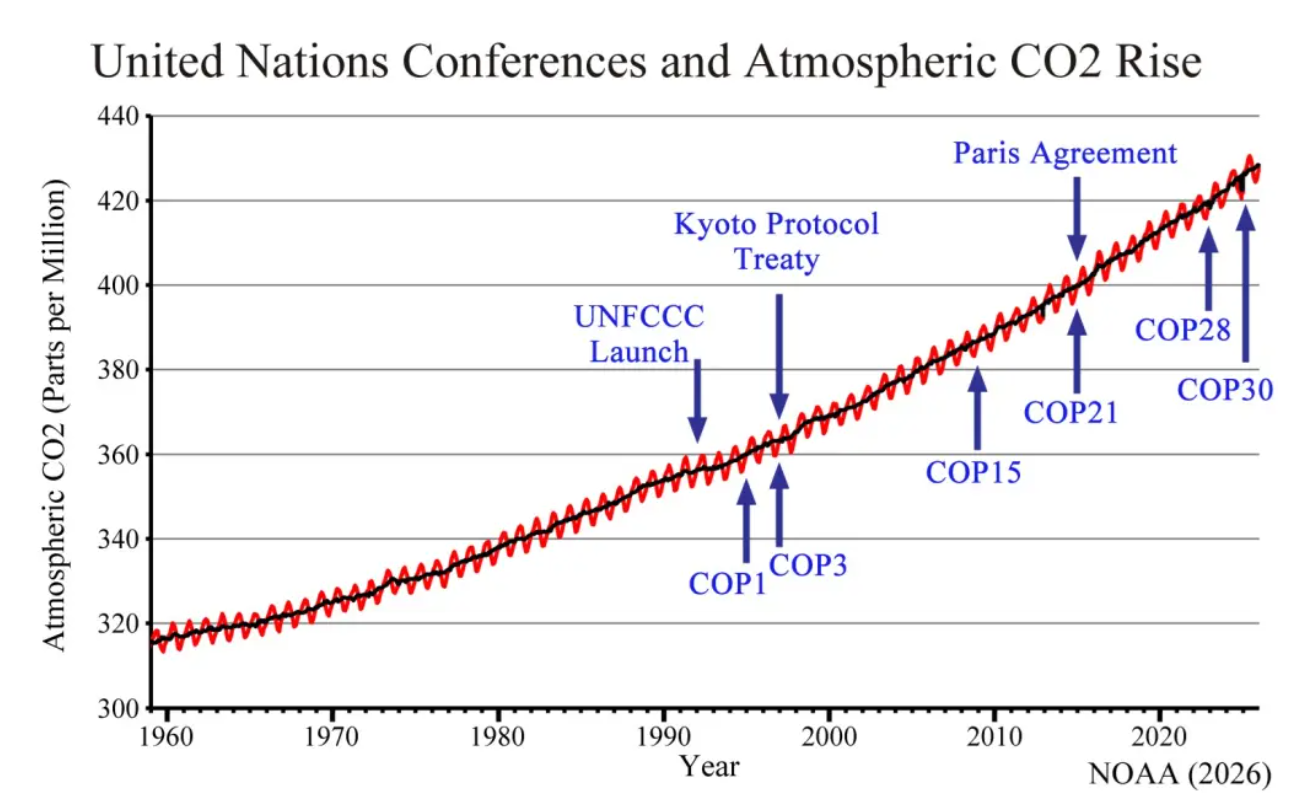

Delegates at the first World Climate Conference held in 1979 adopted a declaration calling on governments to “foresee and prevent man-made changes to the climate that might be adverse to the well-being of humanity.” It was, in effect, a declaration of war against the oil and gas industry.

At the time, I was the president of a Calgary-headquartered oil and gas company that I had co-founded, as well as volunteer-president of our industry’s public communication vehicle, the Independent Petroleum Association of Canada. My industry colleagues were reluctant to take on the global climate elite, but I believed doing so was vital to the future of our industry, which was the bedrock of western Canada’s economy. My public commentary was, of course, condemned as evidence that I was only out to save the oil and gas industry.

But it wasn’t just my responsibility as an industry leader that called me to challenge that World Climate Conference declaration. I knew that extremely hot temperatures had been occurring long before that first Kyoto conference. For example, in the 1920s European immigrantssettled in the verdant grasslands of southeastern Alberta. Some of those hopeful settlers were my wife’s grandparents. A decade later, rain stopped falling and temperatures soared as high as 43 C. Hot, dry winds blew precious topsoil away, spawning choking dust storms. The “Dirty Thirties” had arrived. Starving settlers turned to eating rabbits, gophers and anything else edible they could scrounge. Parents took their kids to school in blinding dust storms, clutching fencelines and breathing through bandanas. And the wind kept blowing through the long, cold Alberta winters. Contrary to net-zero zealots’ rhetoric, half of Canada’s 20 hottest days pre-dated that 1979 World Climate Conference.

World Climate Change Conferences continued during the 1980s and 1990s, each featuring more alarmist rhetoric than the last. At the 1997 conference in Japan, 37 industrialized countries adopted the “Kyoto Protocol,” which committed them to reducing green-house gas emissions to five per cent below 1990 levels by 2012. The war on fossil fuels was on in earnest, and it was destined to escalate to ridiculous heights. At the 2012 conference in Qatar, the rich countries committed to reducing emissions by at least 18 per cent below 1990 levels by 2020.

The naivety of those targets is breathtaking. Countries accounting for over half of global emissions, including China, Russia and India, continued their rapid growth without constraint. Virtually all other Asian, Middle Eastern and South American nations had no intention of playing the Kyoto game. Their emissions were going nowhere but up.

The 22nd climate conference was held in Morocco in November 2016, a year after Canadians elected the Trudeau government. In keeping with the new prime minister’s zealous embrace of the cause, environment minister Catherine McKenna led a delegation of 225, one of the largest among the 100 countries assembled. That cost taxpayers a lot in emissions-spewing flights!

Imagine our delegation’s shock when, just 24 hours after the conference opened, they heard the soon-to-be 45th U.S. president, Donald Trump, declare that man-made global warming was a “big hoax” promulgated by China and other countries wanting to steal American jobs.

With all the major players sidelined, who was left to save the planet from climate Armageddon? Just the EU, Japan and Australia, with a combined emission share of 15 per cent. And Canada, adding our minuscule 1.6 per cent. But futility didn’t deter the Trudeau government from saddling Canadians with carbon taxes and taxpayer-funded wind and solar power subsidies in pursuit of its “net-zero” holy grail.

Now we have a new prime minister who is trying to appear less committed to the net-zero mission. But the transformation of the UN Secretary General’s “special envoy on climate action and finance” has been less than biblical. True, one of his first actions on taking power was to remove the despised consumer carbon tax. But that was largely sleight-of-hand, moving the tax out of public view onto beleaguered businesses already struggling with Trump tariffs.

Meanwhile, the foundations of the net-zero emissions religion are crumbling rapidly. In 2021, Microsoft founder Bill Gates wrote a pro-carbon tax book entitled “How to Avoid a Climate Change Disaster.” But four years later, in a letter published on the eve of the most recent UN COP conference, he advised, “too many resources are focused on emissions and the environment. More money should go toward improving lives and curbing disease and poverty.” And he called out the “doomsday view” of climate change, urging world leaders to make a strategic pivot and focus on issues that “have the greatest impact on human welfare.”

Net-zero fatigued Canadians should be asking their prime minister, “Why are you weakening our already struggling economy with carbon taxes and wasting taxpayer money subsidizing wind farms when it will make no perceptible difference to the global climate?” He owes them an answer.

Turns out that concern for mankind’s effect on the global climate isn’t much of a concern at Davos this year. It is, after all, the meeting of the World Economic Forum, not the World Climate Forum – the United Nations already has a forum for climate change, and it drew a lot of ignoring this year, too. This year in Davos, Switzerland, though interest in all things climate seemed to be nearing an all-time low.

A recent article at Climate Change News discussing this week’s 2026 World Economic Forum (WEF) meeting in Davos, Switzerland worries that climate change is no longer a high priority for the attending global elites, while also attempting to reassure readers that the topic hasn’t disappeared entirely. It is true that climate change is dropping on the list of elites’ concerns, but it is not a bad thing. The attendees’ concerns are still wildly out of step with the concerns of average people who are impacted the most by the policies discussed and pushed at Davos.

The article, titled “Ahead of Davos, climate drops down global elite’s list of pressing concerns,” was written before the Davos event kicked off Monday, January 19, and focuses on a survey conducted by the WEF’s Global Risks Perception Survey of “experts” and leaders in advance of the meeting. This year, the survey found that for the first time in years, “climate change, pollution, and biodiversity loss have dropped down an international ranking of short-term concerns for high-profile business leaders, academics, and politicians,” as priorities shifted towards more concern over “economic risks like geoeconomic confrontation, economic downturn, inflation, and asset bubbles bursting.” (See the graph, below, from the WEF).

That’s a novel notion. An economic forum worried about economics.

Oh, the climate can have an effect on economics; there’s little doubt about that. A real humdinger of a climate crisis, like a major volcanic eruption, can have dramatic effects on everything from agriculture to fisheries, and if people can’t eat, they have little time to worry about anything other than keeping their belly buttons from rubbing a hole in their backbones.

As far as possible reasons for the shift, a polling form often used by the WEF found that this year the general run of citizens – you know, the people who elect a lot of the “elites” at Davos – are a lot more worried about the price of eggs than their carbon footprints.

Personally, I’d prefer to think that people are just figuring it out.Unless a government is willing to go full Great Britain and tell the subjects – the Brits, we remind you, are not citizens, not as we think of the word – and say, “You’ll have your electric cars and heat pumps, and you’ll bloody well like it or else,”then people just aren’t seeing the point. Giving up the gas stove, the SUV, and the comfortable, gas-heated home, just to keep the Earth’s mean temperature from rising by a degree and a half over the next century? Plenty of regular folks aren’t buying the hype. They just don’t see what the big worry is, and the people at Davos must be wetting their fingers and holding them aloft, because it sure seems like they know which way the wind is blowing.

Thomas Kolbe reports on a major turnabout in his American Thinker article Hour of the Opponents in Davos. Excerpts in italics with my bolds and added images.

Machiavelli is dead, long live freedom.

Wednesday was the day of the opponents at the annual World Economic Forum gathering in Davos. Donald Trump and Argentina’s Javier Milei tore apart the WEF agenda. One declared globalism as officially failed, the other wielded an intellectual-ethical scalpel through the decayed body of the establishment.

Norwegian Børge Brende has been the chairman of the World Economic Forum since last year. He took over after a heated internal personnel debate from the WEF’s founder, Klaus Schwab, who for decades dominated the agenda of this shadowy institution for political will-shaping.

Schwab did so with undeniable success. The WEF has become an ideological melting pot of European politics, from which socialist concepts long proven costly in blood and failure continue to resurface — now repackaged as morally renewed, dressed in green.

Whether it’s the EU’s climate-socialist agenda, peculiar ideas like the 15-minute city to restrict individual mobility, or digital control currencies designed to make hidden capital controls palatable — the WEF has always been a source of centralist fantasies of political power.

Fleet of Teslas at WEF Forum

Take the vision of the digital identity of the new global citizen, who no longer exists as an individual but as a managed dataset — this too originates in Davos think tanks. Every person would possess a centralized, supranational digital existence where financial behavior, health status, and political reliability are consolidated into a controllable unit. The culmination of the “transparent citizen,” the final chapter of individual dignity and freedom.

Mobility, nutrition, housing — all are turned into moral tests. The CO2 footprint replaces personal judgment; deviation is social misconduct. Davos has grown in the haze of its control fetish into the symbol of a leadership claim by a detached pseudo-elite.

Hour of the Antagonists

Informal political organizations like the WEF live on media presence. Continuous coverage is their lifeblood, which makes inviting the most powerful political figures — like U.S. president Donald Trump or South America’s rising star, Argentina’s Javier Milei — practically inevitable.

Brende, Schwab, and the roughly one thousand invited guests

surely anticipated what the appearance of the two might bring.

And they were not disappointed.

Trump, outside his MAGA orbit hardly known as a master orator of refined rhetoric, declared the World Economic Forum agenda officially failed in his own unmistakable way. He mocked European energy policy, spoke openly about the continent’s self-destructive migration policies, and presented an US economic record that made even seasoned technocrats sit up:

♦ 5.4 percent growth in the last quarter, ♦ full deregulation of the energy sector, and ♦ a radical downsizing of the federal bureaucracy by 250,000 employees.

Advertisement

These were blows to the heart of central planners and declared friends of the “big state.” Heavy on main clauses and rich in imagery, Trump dismantled the Davosites’ fantasies of omnipotence one by one. Planning versus growth, moralism versus prosperity, control versus dynamism — every certainty was exposed like a warped political myth.

His ultimate checkmate came with the sober reminder of Europe’s total dependence on the American military apparatus. Those who cannot defend themselves, the unstated message implied, should be cautious in delivering moral lectures. Greenland salutes.

The outraged media response that followed proves one thing: he hit the mark. And, in essence, did nothing less than openly lay out the conditions of this system’s potential capitulation.

Milei Delivers an Ethical Bankruptcy

Where Trump brought a rhetorical sledgehammer,Milei immediately followed with the elegant intellectual foil. The organizers had clearly hoped to tone down the disruption of their feel-good gathering by seating the two opponents consecutively. But the double act only amplified the effect — and the message.

Milei opened with a jarring statement: “Machiavelli is dead.” Its meaning, however, was unmistakable. The politics of public manipulation and technocratic governance, which have become a guiding principle in EU Europe, do not lead to order but to their own crisis. The state, Milei insisted, must beguided by moral principles and make individual liberty the starting point of political action.

This was the maximum confrontation with the WEF agenda.

The gauntlet had been thrown.

He pressed further. One hundred fifty million people, he alleged, had lost their lives in the name of socialism over the past century; the survivors lived in poverty. Justice, he argued, belongs only to free-trade capitalism: voluntary exchange and the absolute respect for property rights, founded on meritocratic values. This is the recipe for a prosperous civilization.

These words carry weight. In two years, Milei literally turned the helm of his nation: he restored Argentina to growth, radically cut the bureaucracy, and brought inflation under control. Who would have expected that intellectual rigor and ethical grounding could one day inhabit the presidency of a nation as significant as Argentina?

Milei also answered the crucial question of our time:

How can the current cultural crisis be overcome?

Only by returning to the sources, he diagnosed — Greek philosophy as the inspiration of thought, Roman law, republican principles, and above all Judeo-Christian values. Together, these civilizational achievements form the recipe for a Western comeback.

Real wages for Argentina’s registered private sector workers reached 107 on the index (base 2023=100) in February 2025, the highest since August 2018, according to the Observatory of Employment and Business Dynamics.

Milei did not miss an opportunity to deliver a late retort to German chancellor Friedrich Merz. A year ago, Merz had called Milei a politician who tramples his own people and promotes a divisive agenda and continues to foster an anti-business climate. For Milei, however, entrepreneurs are precisely those who drive the innovation of a free-market economy. Politics must stop harassing those trying to build a better world.

In this light, Merz and his government are indeed a burden for anyone striving forward in life, living by values, and resisting the rhetorical trap of vulgar WEF-style socialism.

The Turning Point Has Arrived

Trump and Milei are merely the most visible representatives of an increasingly influential conservative turn. Even if the European press still portrays the American president as a deranged villain and destroyer of a socialist utopia, the message he and Milei deliver is gaining traction.

The cultural and economic crisis of our time is above all a crisis of statism and faith in the strong state. Its seductive arts inevitably lead to megalomania and scenarios of submission — with the civilizational fracture we see today as a consequence.

In Argentina and the United States, the repair work is already underway.

The open question is no longer whether a course correction is possible,

but when Europeans will follow the example of these two.

For those who prefer reading, below is an excerpted transcript lightly edited from the interview, including my bolds and added images.

Hey everyone, it’s Andrew Klavan with this week’s interview with Bjorn Lomborg. I met Bjorn, he probably doesn’t remember this, but I met him many, many years ago at Andrew Breitbart’s house. Andrew brought Bjorn over to talk in LA and I listened to him talking about all the simple and inexpensive things that could be done to make actual change and do actual good in terms of climate change, which I think at that point was still global warming.

And you know, we had a small audience, and I asked the question, well, if these are so such smart, cheap ideas, why don’t politicians do them? And Bjorn said, well, because that wouldn’t give them the chance to display their virtue. And I thought, here’s a man who not only knows about science, but actually knows about human nature. And I’ve been following him ever since.

He is a president of the Copenhagen Consensus Center, a visiting fellow at Stanford University’s Hoover Institution, an author of False Alarm and Best Things First, the best writer, I think, on climate issues and other issues. Bjorn, it’s good to see you.

Andrew, it’s great to be here. And I do remember that event, although I remember it for seeing the guy who played on Airplane. Sorry. So I remember that because it was it’s still one of my favorite movies. It’s one of the greatest movies ever made, I think. It really is very, very funny. Yeah.

On a totally different direction. So I was watching with great approval Donald Trump’s appearance at the United Nations. I guess it would be when we’re playing this last week. And he he had this. I’m just going to read just a little bit of the speech. He said in the 1920s and the 1930s, they said global cooling will kill the world. We have to do something.Then they said global warming will kill the world. But then it started getting cooler. So now they could just call it climate change because that way they can’t miss if it goes higher or lower, whatever the hell happens. It’s climate change. It’s the greatest con job ever perpetrated on the world, in my opinion. Do you agree with that?

So I get where he’s coming from. And I think there’s some some truth to this. I mean, Donald Trump always speaks in larger than real life words. Yes. So it’s not a con job. There is a problem. And actually, in some sense, bizarrely, as it may sound, you know, the world is built all of our infrastructure is built to live at the temperature that we’ve had for the last hundred or two hundred years. That’s true in Los Angeles. That’s true in Boston. It’s true everywhere in the world. And so if it gets colder or if it gets warmer, that will be a problem. So there is an issue here.

But obviously, it’s vastly exaggerated when people then talk about the end of the world. You may remember that this was one of the favorite terms of Biden, but not just Biden, but pretty much everyone for the last four years and certainly more as well. That this is an existential crisis. There was a recent survey by the OECD, so in all rich countries in the world, where they found that percent of all peoplebelieve that unmitigated climate change, so climate change we don’t fix, will likely or very likely lead to the end of mankind. And that, of course, is a very different statement.

There is a problem, that’s true. It’s not the end of the world. But the end of the world is a great way to get funding.

And that’s why people are playing it out. But it doesn’t make for good policy. Remember, if you think the end of the world is near, you’re going to throw everything in the kitchen sink at this, which, of course, is what the campaigners would like you to do. But you will probably waste an incredible amount of resources because you’re just going to try everything.

Climate change is a problem. So I disagree with Trump there. But yes, there is an incredible amount of exaggeration. And I agree with him there. So there’s I mean, the climate changes but we’re not living in a glass bubble. And we’ve even in I don’t know, I guess it was the late 19th century, the Thames in London froze over and people went skating on it. It’s so there are these big changes and there have been ice ages, obviously. How much of this or do we know how much of this is is caused by human beings?

I have to preface this with saying I’m a social scientist, so I work a lot on the costs and the benefits of us doing policies against climate change. I’ve met with a lot of the natural scientists who study all this. Please don’t do this at home, but I’ve read the UN climate panel report, most of the pages, not all of them. And it’s incredibly boring, but it’s also very, very informative. So so I have a reasonably good take on this. And what they tell us is that the majority of the recent warming that we’ve seen is due to climate change.

I have no idea to evaluate that, no way of independently evaluating that is due to natural climate change or is manmade, due to mankind. So is it mostly due to us emitting CO from burning fossil fuels?

So there is a significant part of what’s changed over the last century or thereabouts, which is about two degrees Fahrenheit or one degree Celsius. So that’s something and that’s something we should look at. But also, we should get a sense of what’s the total impact of this. Well, actually, climate economics have spent the last three decades trying to estimate: what’s the total cost of everything that happens with climate change.

So, you know, there are lots of negatives. There’ll be more heat waves. There’ll possibly be stronger storms. There’s also going to be fewer cold waves, which is actually a good thing. There’s also going to be CO2 fertilization. So we’ll have more greenery. You know, if you add all the negatives and all the positives, it become a net negative. That’s why it’s a problem. But also get a sense of this.

If you look across all of the studies that we’ve done, we estimate the net negative impact today is about 0.3% of GDP. So yeah, a problem, not the end of the world. And it’s crucial to say, if you look out till 2100 which is sort of the standard time frame, which is a long time from now, we estimate if we do nothing more about climate change, so we end up with three degrees Celsius, so about degrees 5.6 Fahrenheit, then the cost will be about to 2 to 3% of global GDP every year.

That’s certainly not nothing. That’s a lot of trillions of dollars. But again, it’s 2 to 3%. It’s not, you know, the end of mankind, It’s not anywhere near a hundred percent. And this is not me saying this. This is the guy William Nordhaus from Yale university, the only guy to get the Nobel prize in climate economics. And Richard Tol one of the most quoted climate economists in the world. They’ve done separate studies. One to find 2%, the other one to find 3%. That’s the order of magnitude we’re talking about. And just for, for added emphasis, remember by then everyone in the world will be much, much better off.

Just like if you compared people from back in 1925 and until today, the UN on its standard trajectory estimate, the average person in the world by the end of the century will be somewhere around 450% as rich as he or she is today. That’s not the US that will. And you know, people come from Denmark and other rich countries might only be 200% as rich, but many in Africa and elsewhere will be a thousand percent richer. So on average, because of climate change, it will feel like they’re only 435% as rich, which sort of emphasizes, yes, that’s a problem. I would rather have a world that’s 450% as rich trather than one that’s 435%. But it’s not the end of the world.

It’s still a fantastically much better world, just a slightly less fantastically much better world. And that less money that people will have will mean less money you have to spend, what, shoring up buildings. And so the way they measure that is actually in equivalence of how much you would need to get compensated to live with the problems.

So we don’t actually look at whether people will fix it or not. You know, it’s a bit like, if you have a slightly dangerous job, you get more money. And that’s basically a way of saying, but you’ll also have to live with that constant slightly higher risk of dying. Right. So we’re compensating you for that. That’s the, that’s the amount that we’re talking about. So it’ll feel like you’re only % as rich, although you’ll probably in reality, get all that, that slight extra money to get up to 450%, but then you will also have to live with some problems from climate change.

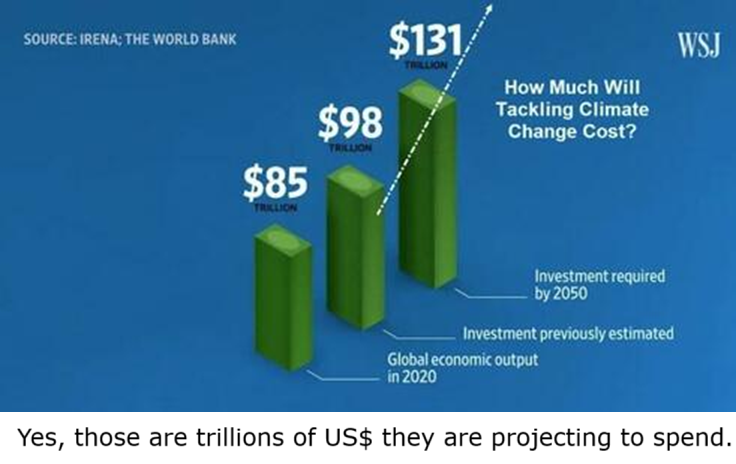

This week I was arguing with a socialist, lovely guy, but just the guy who believes that like all money should be redistributed. And I was pointing out that this was giving a lot of power to the people in power. And one of the things I sent him was this article you wrote in the, in the New York Post, which was exactly the kind of article that makes me angry. And I mean, it makes me frustrated with our politics. I want to read just a couple of sentences. Last year, the world spent over $2 trillion on climate policies. This is Bjorn Lomberg writing in the New York Post. By 2050 net zero carbon emissions will cost an impossible $27 trillion every year. So this, this will choke growth, spike energy costs and hit the poor hardest and still will deliver only 17 cents back on every dollar spent. Meanwhile, mere billions of dollars could save millions of lives. I’d like to take this apart a little bit, but to begin with all the stuff that we are spending this money on, is it doing anything? Will it have any effect?

It will. I mean, what, what are we spending money on and what will it do? So these $2 trillion, that’s sort of the official number from the International Energy Agency and many others. It’s a very soft number because obviously what goes into all this money, surprisingly, it’s also all the cost into EVs or electric cars, which of course gives you a thing that can drive you from place A to B, at least if it’s been charged. So, I mean, there are some benefits to this. It’s also spending on solar panels and wind turbines, which again, obviously gives you electricity when the sun is shining and the wind is blowing. It actually also gives you higher electricity costs all the other times, because you now need to have backup power for when it’s not shining or windy, and that capital is being used less.

So there’s a lot of spending, it’s a very big headline number. There’s $2 trillion, everyone uses it, but it, but it’s not all that informative, because the global economy is about a hundred trillion dollars. It means we’re spending 2% on stuff that we probably wouldn’t have done had we not been scared witless on climate change. And that’s a waste. I mean, remember the total spend on healthcare is perhaps 8%. The total spend on education globally is about 5%.

These are big numbers. This is something that could have done a lot of good elsewhere. But I think the real point here is to say people want to take us to a cost that’s much, much, much higher. Remember all the world’s governments, almost all the world’s government now, not Donald Trump and the US, but most governments have pledged in one form or another that we’re going to go net zero around 2050 or shortly thereafter. But nobody looked at what the cost of this will be, which is a little surprising. Because the numbers I’m going to show you suggest that this one single promise is about a thousand times more expensive than the second costliest policy to which the world has ever committed, which was the Versailles treaty back in 1919, had Germany actually paid all the money it was supposed to. That cost was about half a trillion dollars in today’s money, which of course is why Germany never paid it. But now we’re talking about something that is going to be in the order of a thousand to two to 3000 times more costly.

Yet nobody’s looked at what the cost will be and what will be the benefits?

There’s no official estimate of this.

So two years ago, a professor from Yale university, Robert Mendelsohn, gathered a lot of really smart climate economists to try to estimate what’s the cost, and what’s the benefit of net zero. A lot of those really, really smart economists ended up chickening out. You can understand why it’s a really hard question. You’re also asking what will happen in the next hundred years and you’re trying to put estimates on it. At the end of the day, they published a big study published in the journal of climate change economics, which is a period article.

And they had one benefit estimate and three cost estimates. So this is obviously not great, but it’s the only thing the world has. And so that gives you a sense of how much will this cost and how much good will do. If you take the average of these three cost estimates, that gives you $27 trillion in cost per year throughout the 21st century. That’s where that number comes from. $27 trillion. So that’s about a quarter of global GDP right now, because we’re going to be much richer, that is only going to be about 7% of global GDP across the 21st century. But you know, that’s an enormous cost that’s on the magnitude of bigger than education, a bit smaller than healthcare and for everyone in the world, that’s a lot of money.

Now, if this gave you a lot of benefits that might be worthwhile. I mean, we pay a lot of money for stuff that’s good, but we’ve already established that even if we could entirely get rid of climate change, it would only reduce costs by two to 3%. So spending 7% to get rid of two to 3% is a bad deal, but unfortunately net zero by 2050 means we’ll only get rid of part of it, right? Because we’ll already have cost a lot of climate change. So the net benefit is only about 1% of GDP across the century or about four and a half trillion dollars.

So there’s a real benefit. That’s why climate change is real. There’s a real benefit to net zero, but the benefit is much, much lower than the cost. So $4.5 trillion in benefits, $27 trillion in cost every year in the 21st century, we’ll be paying much, much more than the benefits will generate for the world. That’s just a bad deal. There’s no other way to put it.

And the fact that we’re not honest about this and that most people just are not honest about it is one of the reasons why we’re wasting money and spending it so badly. The last bit of the quote that you just said was we could do so many other good things. Remember, most people in the world are not living in nice countries like the US or Denmark. Most people are not considering, you know, the biggest problem which of the many programs and series they want to follow are, am I going to take first or watch first? Or, you know, what kind of takeout am I going to have? They worry about their kids dying from easily curable infectious diseases, not having enough food, having terrible education, not enough jobs, corruption, all these other things. And the truth is we could solve many of these problems, not all of them, but many of them to save millions of lives at a fraction, a tiny, tiny fraction of this cost. So instead of talking trillions, we’re talking billions.

Why is it that we’re so obsessed with spending trillions to do almost no good a hundred years from now, instead of spending billions and doing a lot of good right now to avoid people dying from tuberculosis and malaria, avoid people having terrible education, getting better economies, all these things that we know work at much lower cost. That’s my central question to all these feel gooders. I mean, I know that they want to feel good about themselves, but in some sense, I would like to believe that they actually want to have done good at the end of the day.