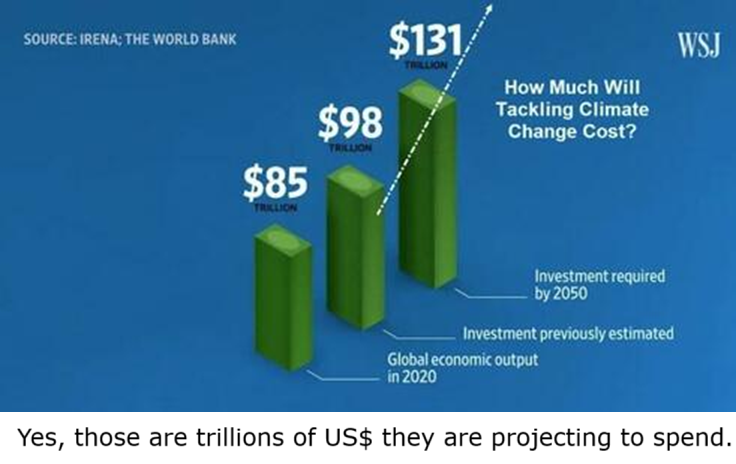

World Dodged UN Climate Bullet, thanks to US

Matthew Boyle breaks the news at Breitbart Mike Waltz Reveals How Trump Killed ‘Global Green Tax’ That Would Have Created ‘U.N. Climate Slush Fund’ at 11th Hour. Excerpts in italics with my bolds and added images.

NEW YORK — U.S. Ambassador to the United Nations Mike Waltz told Breitbart News exclusively of how President Donald Trump and his cabinet rallied at the 11th hour to thwart globalists from creating a “global green tax” that he argued would have created a “U.N. climate slush fund.”

“They were this close to mandating that we basically have a Green New Deal in our global shipping fleet,” Waltz told Breitbart News on the floor of the U.N. General Assembly in the interview taped on Thursday, Oct. 23. “Eighty percent of our economy is based on trade. It would have been devastating. In fact, it would have added a billion dollars a month to the cost of sending our goods around the world or receiving goods. We got fired up as a cabinet — the EU, Brazil, and others thought this thing was a done deal. We got everybody involved, including the president. He came in off the top ropes, and we defeated that vote. I think we just saved the American consumer a massive, massive — what would have been the first U.N. tax in global history just this past week. So that’s the kind of fighting that we’re doing in the types of these organizations, and the kind of wins that we have to deliver for the American people.”

Waltz further explained that the tax that would have been created would have targeted U.S. ships and forced them either to pay billions in global taxes or go through retrofitting in China to use European-backed power sources — but ultimately this has been stopped. He does expect the globalists who pushed this effort to try again, but he said next time the Trump administration will be even more prepared and will stop it again.

“If we had coal fired, gas fired, oil fired ships, this global organization was going to impose a fine on those shipping companies, of course, and that would have been to the tune of a billion dollars a month globally that would have been passed on to the consumers, obviously,” Waltz said. “That money then would have would have formed a U.N.-run green climate slush fund to the tune of $12 to $15 billion a year that would have turned around and done more and more of this. It really would have been the first global green tax and I think we would have felt it through inflation. We would have felt it on our consumer shelves and it would have been yet another assault on the American oil and gas industry.

Published by European Maritime Safety Agency

“We said there will be consequences if you do this and we laid out what those consequences were. Now, we were accused of being diplomatic gangsters and bullies and what have you. But look, it was they who are being the climate bullies and we’re not going to allow them to do that to our shipping fleet. If it had happened, here was the real secret. The EU was subsidizing all the biofuels that they wanted to push to our ships and the only place we could retrofit our ships were in Chinese ports and shipyards. So this would have been a win for the EU, a win for China, a loss for the United States. We said, ‘We’re not going to have it,’ and we got in there and won.”

So, are they trying again? Of course they’re going to try again. As we came at this, frankly, a little bit last-minute, we won, but we delayed the vote until next year. We’re going to make our position crystal clear, and I don’t think this thing is going to get through now. This is just the tip of the iceberg. It’s what’s happening in these over 80 organizations around the world. What it really amounts to is a climate ideology that is nonsensical. It’s an ideology that just doesn’t make sense. For example, in AI [artificial intelligence], a big piece of that is power. You can’t power AI through wind and solar — you just can’t — and we already know the President’s problems with wind. We already know that the vast majority of solar panels are made where? In China.

But we need an all-of-the-above solution. We need nuclear, we need gas, we need oil, we need coal, and those other renewable forms of energy in order to win. But what we find is even when we reach, say, some kind of trade deal with a country or with the EU, then they try to back door these regulations in favor of them and against us through these international organizations that are often under the U.N. umbrella. That’s why we need fighters in here. I have Tammy Bruce who will be going to the Senate to be the Deputy Ambassador here. We have myself, and we have other members of the team that 100 percent believe in the President’s America first agenda. We’re going to start fighting and blocking and tackling in these organizations.”

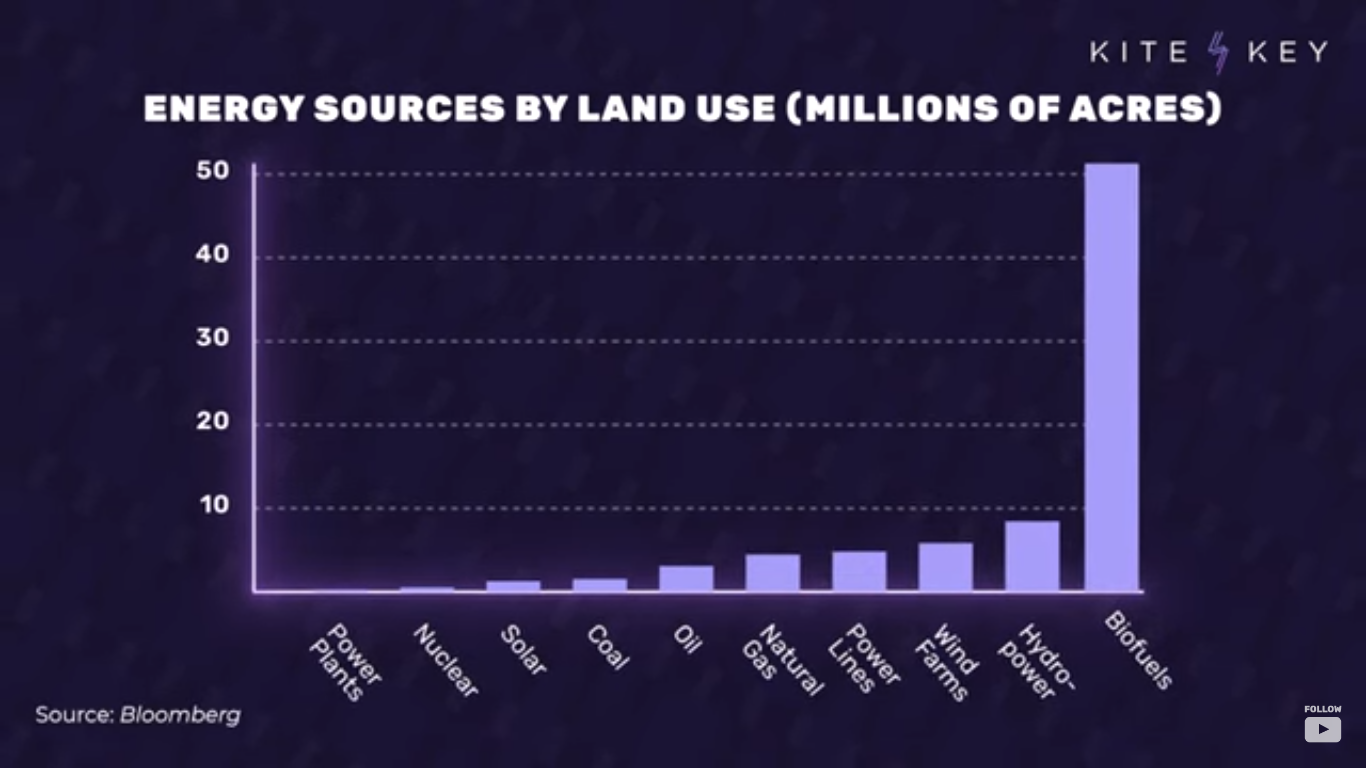

Addendum on Biofuels, the worst energy choice, disqualified for “All of the Above”

Put simply, power density is just how much stuff it takes to get your energy; how much land or other physical resources. And we measure it by how many watts you can get per square meter, or liter, or kilogram – which, if you’re like us…probably means nothing to you.

So let’s put this in tangible terms. Just about the worst energy source America has by the standards of power density are biofuels, things like corn-based ethanol. Biofuels only provide less than 3% of America’s energy needs–and yet, because of the amount of corn that has to be grown to produce it … they require more land than every other energy source in the country combined. Lots of resources going in, not much energy coming out–which means they’re never going to be able to be a serious fuel source. Moreover, it cannibalizes arable land needed for food.