Biden’s EV Boondoggle Enriches Himself

The Greenest thing about the New Green Deal is the Money.

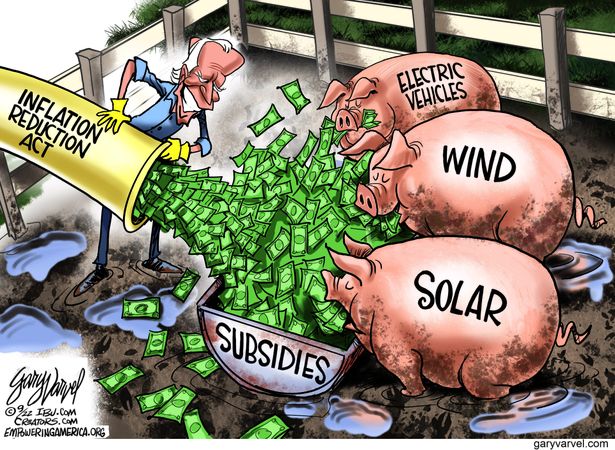

The spending on “Green Energy Projects” is enormous and uncontrolled. Larry Behrens explains at Real Clear Energy Too Favored to Fail:” Taxpayers Bailout Biden’s Green Friends. Excerpts in italics wtih my bolds.

While America struggles to buy groceries, President Joe Biden has a

green slush fund worth billions of dollars, and he’s not afraid to use it.

Billions Disappear with Rivian Bankruptcy

Recent revelations uncovered that the CEO and lobbyists of Rivian, an electric vehicle manufacturer, held a quiet meeting at the White House with Biden’s Climate Czar, John Podesta. That’s right, the same John Podesta who served as chairman of Hillary Clinton’s ill-fated 2016 presidential campaign before being pulled from the ranks of profitable green consulting to oversee distribution of $369 billion from the Inflation Reduction Act (IRA). Biden selected a political operative with green company ties to dole out the goodies from one of the largest slush funds in history. Now green CEOs who are hemorrhaging cash are beating a path to his White House office, presumedly with hat in hand.

According to media reports, Rivian is deep in the red. Last year, they lost $6.8 billion. In 2021, it was $4.7 billion, which is in addition to the $1 billion lost in 2020. These massive losses happened as EV manufacturers enjoyed large subsidies both to build and sell their vehicles. In fact, President Biden went out of his way to praise Rivian in early 2022, even though their stock had already lost half its value on its way to losing 87% of its value since 2021. Losing over $12 billion in less than three years would normally be a problem in the business world, but in the upside-down reality of Biden’s green agenda, that gets you a meeting at the White House.

Tax dollars are flowing from the IRA so quickly that the Department

of Energy’s Inspector General (IG) may be running out of adjectives.

Earlier this month in testimony before the Senate, the IG said, “the current situation brings tremendous risk to the taxpayers.” Red flags about American dollars flowing to foreign companies or just being wasted here at home are going up, yet according to budget watchdogs, their concerns are met with deaf ears by senior Biden Administration officials. The IG notes there were “billions and billions of dollars lost or stolen” from federal Covid funds, and Biden’s slush fund is even bigger. To put it bluntly, the green vault is wide open and the grifters are lining up.

“Green Banks” Dole Out Taxpayer Cash

Here’s a particular galling example. One little known aspect of the IRA are so-called “green banks.” For greenies, the scheme is simple: regular banks will not fund their boondoggles, so they need a taxpayer backed entity to dole out cash. Unlike regular banks, these green banks do not need to make a profit to stay afloat because the government is their funder.

New Mexico Governor Michelle Lujan Grisham was caught trying to set up a green bank without the trouble of going through the elected legislature. The board of the bank will be green non-profits who will be in charge because as the New Mexico climate czar put it, “We’re talking about hundreds of millions of dollars…This greenhouse gas reduction fund is a remarkable little beast.” Recently, Grisham announced the green bank anyway. The slush fund is open for business, and everyone has their hand out.

Congress is watching the “green bank” scheme because they know it is ripe for abuse. The problem is clear: The White House put a political operative in charge of what is nothing more than a political fund. For Barack Obama, they were too big to fail, but Joe Biden is taking it further. When it comes to his failed agenda, his green boondoggles are “too favored to fail.”

Biden’s Wasted EV Subsidies Eclipse Solyndra

Helen Raleigh reports at The Federalist The Biden Administration’s Electric Vehicle Subsidies Are Becoming Another Solyndra. Excerpts in italics wtih my bolds.

Energy Secretary Jennifer Granholm made $1.6 million from

an electric car company the Biden administration boosted

that just went bankrupt.

Proterra, an electric bus and battery company that President Joe Biden touted as a success of his green energy initiative, filed for bankruptcy in August. Last week, it finally sold its embattled battery business at a rock-bottom price as part of the bankruptcy proceeding. The rise and fall of Proterra demonstrates once again that politicians should refrain from betting taxpayers’ money on business ventures to advance their political agenda.

According to the Wall Street Journal, Proterra has sold only 550 electric transit buses since its founding in 2004. Most of the sales were underwritten by government agencies with federal grants. Proterra’s electric buses were plagued with mechanical defects and other performance issues, such as limited range and long charging times. Besides government subsidies, the company only survived as long as it had due to powerful political connections. Former Michigan governor Jennifer Granholm, Biden’s energy secretary, served on its board.

Despite all the quality issues of its EV buses, Proterra went public in January 2021 and raised $650 million, more than three times its annual revenue. A month after the company’s IPO, Biden tapped Granholm as his energy secretary. Proterra’s political connection to the Biden administration paid off in many ways.

Surviving on Grants and Tax Credits

In April 2021, Biden took a virtual tour of a Proterra facility to promote his infrastructure plan. The proposal included $6.5 billion in grants to help replace diesel-powered school and transit buses with electric ones. During the tour, Biden lauded Proterra for “getting us in the game.” He predicted that Proterra and other electric vehicle companies would “end up owning the future.”

Biden’s 2022 Inflation Reduction Act further enriched Proterra’s coffer. The law had little to do with reducing inflation, but it gave massive government handouts to the green energy sector. For instance, IRA includes a $40,000 per vehicle tax credit for purchasing electric commercial vehicles and an additional tax credit for EV batteries.

Proterra admitted in its quarterly report that “the availability of this new unprecedented level of government funding for our customers, suppliers, and competitors to help fund purchases of commercial electric vehicles and battery systems will remain an important factor in our company’s growth prospects.” Proterra’s political profile rose even more after Biden appointed Gareth Joyce, CEO of Proterra, to serve on the President’s Export Council in February this year.

Backed by Biden, Buried by Biden

Excessive government spending under Biden has sparked high inflation rates that were last seen in the 1970s. To bring inflation rates down, the Federal Reserve has aggressively raised interest rates. Higher rates increased production and operations costs for many companies. As legendary investor Warren Buffett famously said, “Only when the tide goes out do you learn who has been swimming naked.” Proterra was one of those companies that had been caught “swimming naked” in this new environment.

The company struggled because it had difficulty passing rising costs on to its existing customers, since most were government agencies with little budget flexibility. Nor could Proterra outsource its production overseas or import components at lower costs. Receiving government grants comes with strings attached. One requirement is that companies like Proterra must produce at least 70 percent of their EV components in America. Proterra couldn’t afford to cut the prices of its EVs to drum up sales.

Finally, Proterra filed for bankruptcy in August. Government subsidies could not offset the financial pressure of rising inflation, higher interest rates, and falling sales. Last week, a Swedish automobile manufacturer, Volvo, bought Proterra’s battery business for $210 million, a great deal considering Proterra was valued at $1.6 billion a year ago.

Another party who got an excellent deal was Granholm. She sold her Proterra shares for $1.6 million last year. They would have been worth nothing if she had held on to her Proterra shares until this

August. The biggest loser of the whole Proterra saga is American taxpayers.

No Good News for Electric Vehicles

Proterra was not the only EV company that went under. Michigan-based Electric Last Mile declared bankruptcy in June 2022. Ohio-based Lordstown Motors went bankrupt a year later. Ironically, these companies benefited from the Biden administration’s climate handouts, but the economic consequences of the same policies eventually doomed them. Even large automobile companies’ EV units are struggling. Ford estimates it will lose $3 billion this year on its EV business. The company relies on sales of gas-powered vehicles and government subsidies to keep the EV business afloat.

What’s In This for the Bidens?

Fred Lucas explain in his Daily Signal article Hunter Biden’s Cobalt Deal With China Increases Cost of His Father’s Push for Electric Cars. Excerpts in italics with my bolds.

Presidential son Hunter Biden’s most recent controversy—assisting a Chinese company’s purchase of a large cobalt mine—is linked directly to a top Biden administration policy of promoting electric vehicles.

Cobalt, a relatively rare and expensive mineral, is an essential part of batteries used to power electric automobiles. The COVID-19 pandemic also made U.S. officials and the public much more aware of Communist China’s control of the supply chain for drugs and other products.

The younger Biden, 51, is a one-time partner in China-based Bohai Harvest RST, known as BHR, and reportedly remains a stakeholder.

The New York Times first reported over the weekend that BHR facilitated mining company China Molybdenum’s $2.65 billion purchase of a cobalt and copper mine from an American company, Freeport-McMoRan.

Rep. Ken Buck, R-Colo. told The Daily Signal,

The latest news [that] he assisted a Chinese company purchase one of the largest cobalt mines is another example of Hunter Biden using his influence to line his pockets and help a foreign adversary. Conducting oversight of Hunter Biden’s questionable ethics and dealings that undermine our national security will continue to be a top priority for Oversight [Committee] Republicans.

The committee’s ranking Republican, Rep. James Comer, R-Ky., tweeted: “By helping Chinese companies mine rare minerals in Congo, Hunter Biden is helping Communist China corner the Electric Vehicle market that @POTUS is subsidizing here at home.”

Summary:

The campaign is to force electric vehicles upon Americans who otherwise do not want them. And why? It’s not about climate change, not about the environment. It’s about greed not green.

Stiglitz is simply doubly wrong on his only indication of how Nobel Laureate Nordhaus and I should be wrong, so for the second mistake, Stiglitz makes two false, one unsubstantiated and no correct, relevant claims.

Stiglitz is simply doubly wrong on his only indication of how Nobel Laureate Nordhaus and I should be wrong, so for the second mistake, Stiglitz makes two false, one unsubstantiated and no correct, relevant claims.