Experts Were the Covid Crisis in 2020

John Tamny makes the case that authoritarian government is a poor substitute for free people managing themselves facing a public health threat. He writes at Real Clear Markets Dear Washington Post Editorial Board, the Experts Were the Crisis In 2020. Excerpts in italics with my bolds and added images.

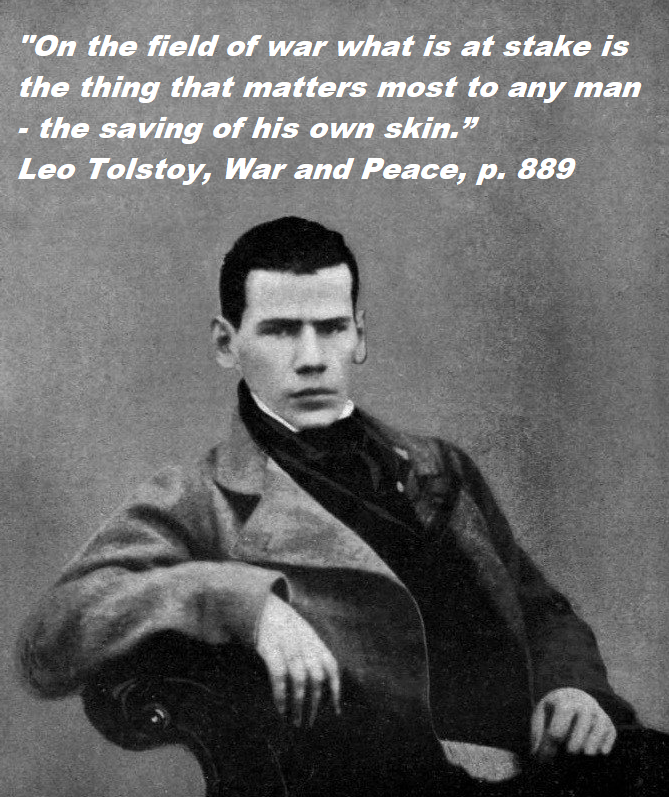

The quote from Tolstoy’s War and Peace is a useful way to begin addressing the Washington Post editorial board’s confident assertion that “’A collective national incompetence in government’” was at the root of the U.S.’s alleged failure vis-à-vis the coronavirus in 2020. According to the Post quoting from a recently released report (“Lessons from the Covid War”), “The United States started out ‘with more capabilities than any other country in the world,’ but “it ended up with 1 million dead.” Were he still around, one guesses Tolstoy would mock the conceit of the Post’s editorialists.

That’s the case because “the thing that matters most to any man” is “the saving of his own skin.” That this needs to even be said speaks to how wrongheaded the Post’s editorial board’s approach to the virus was, and still is. It implies we have dead because government didn’t act properly, as though free people eager to live were unequal to a virus that the right kind of collective governmental action was more than equal to. Ok, but what was government going to do? Better yet, what if the virus had struck in 2015 when Barack Obama was still in the White House. What would he have done? Would he have instructed a virus that was spreading faster than the flu to take a “time out”?

The simple truth missed by the Post is that as humans

we’re wired to preserve ourselves.

On the matter of life and the presumption of death, government is excess. Whatever solution Obama might have come up with, or whatever Donald Trump did come up with, or (try not to laugh) whatever Joe Biden, Nancy Pelosi and Chuck Schumer would have done if the virus had revealed itself in 2021 would have been vastly unequal to the solutions crafted by free people.

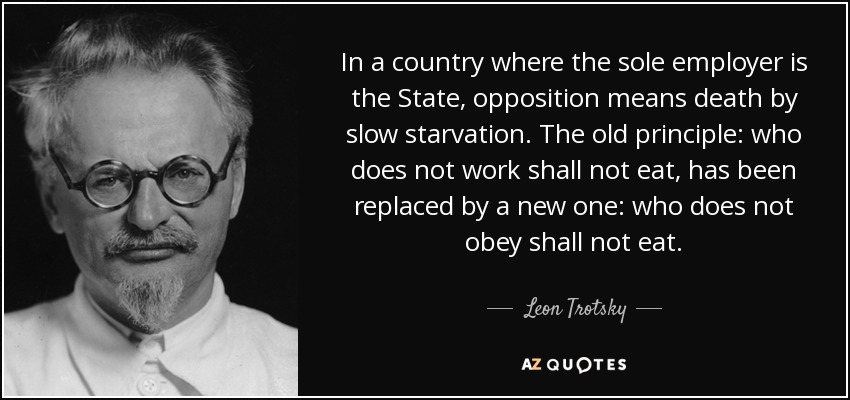

Deep down the Post’s editorialists must know the above is true. Indeed, it’s not that the Soviet Union lacked experts, or that Cuba lacks experts now. The problem was and is that the remarkable knowledge of very few very smart people will never measure up to the collective knowledge of the citizenry. That’s why communism failed so impressively in the Soviet Union, and it’s why it fails in Cuba. Translated for those who need it, the people are the market and markets work. As I make plain in my 2021 book When Politicians Panicked, the problem was experts and politicians substituting their limited knowledge for that of the people. That was the crisis. Not so, according to the Post and the report they cite.

Supposedly the “leaders of the United States could not apply their country’s vast assets effectively enough” such that “1 million died.” Wrong. Over and over again. To see why, imagine if 10 million Americans had died in March of 2020. Can the Post editorial board think of what government might have done that would have somehow improved on a feverish individual desire to survive against long odds? The simple truth glossed over by the Post is that the more threatening a virus is (and the Post seems to view what most didn’t know they were infected with as wildly threatening), the more superfluous government action is.

Really, who reading this ever needs to be forced to avoid behavior that might result in sickness, or even death? And if the reply to this question is that some people DO need to be forced, you’re making the best case of all for unfettered freedom. Think about it. Those who reject expert opinion are the most crucial “control group” as a virus spreads. By going against the grain, we learn from their freely arrived at actions if the virus is as lethal as presumed, or not, how it spreads, how to perhaps avoid its spread, and all manner of other important bits of information suppressed by one-size-fits-all national solutions.

It cannot be stressed enough that free people crucially produce information. Instead of allowing them to produce it in abundance in 2020, the response arrived at by Democrats and Republicans was to lock people in their homes, thus blinding a nation “with more capabilities than any other country” to the best approaches to a spreading virus. Please keep all of this in mind with the report’s assertion that the “most important and fundamental misjudgment” about the virus was how it spread. You think? Of course, the muscular assertion ignores yet again that if knowing how a virus spreads is of utmost importance, the only credible answer is freedom.

Consider the latter in light of the statement of the obvious that all advances in medicine have always been born of matching doctors and scientists with the abundant fruits of wealth creation. In 2020, rather than encourage the very wealth creation that has long been the biggest foe of death and disease (by far), panicky politicians quite literally chose economic contraction as a virus mitigation strategy. Historians will marvel at the abject stupidity of the U.S. political class, but not the Post’s editorialists or the authors of a report that the editorialists remarkably find insightful.

Rather than acknowledge the obvious about government and experts as the crisis, the Post editorialists and the experts they kneel before bemoaned a national abdication of “wartime responsibilities.” One gets the feeling Tolstoy would chuckle yet again. In his words, “The course of a battle is affected by an infinite number of freely operating forces (there being no greater freedom of operation than on a battlefield, where life and death are at stake), and this course can never be known in advance; nor does it ever correspond with the direction of any one particular force.”

In short, on matters of life and death government control

is wretched, crisis-inducing excess.

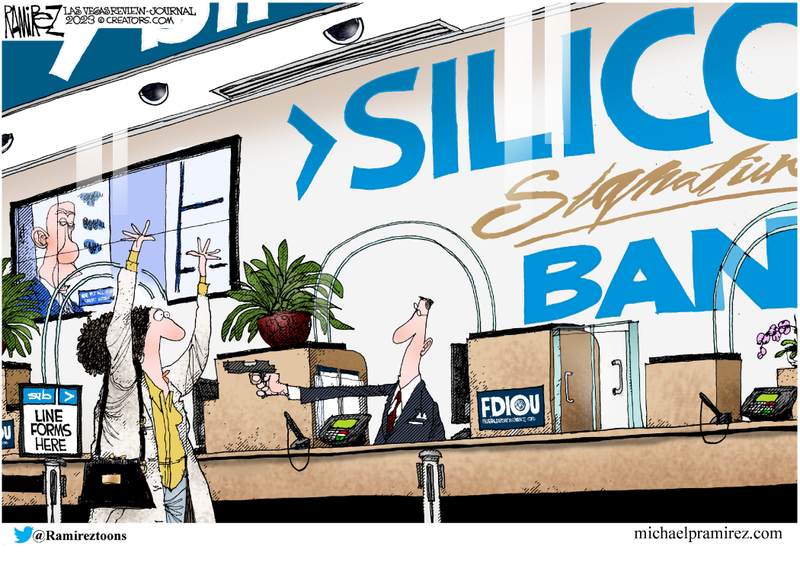

Mish reports on the US Federal Reserve’s latest incompetence at his blog

Mish reports on the US Federal Reserve’s latest incompetence at his blog

Amber Jo Cooper reports at Florida’s Voice

Amber Jo Cooper reports at Florida’s Voice