https://bestwesternsevilleplaza.com/wp-content/uploads/sites/16/2018/05/GettyImages-904008250.jpg

{kind=link}

Most every day there are media reports saying solar and wind power plants are now cheaper than coal. Recently UCS expressed outrage that some coal plants remain viable because industrial customers are able to commit purchasing of the reliable coal-fired supply.

Joe Daniel writes at Forbes The Billion-Dollar Coal Bailout Nobody Is Talking About: Self-Committing In Power Markets. A typical companion piece at Forbes claims The Coal Cost Crossover: 74% Of US Coal Plants Now More Expensive Than New Renewables, 86% By 2025.

Having acquired some knowledge of this issue, I wondered how these cost comparisons dealt with the intermittency problem of wind and solar, and the requirement for backup dispatchable power to balance the grid.

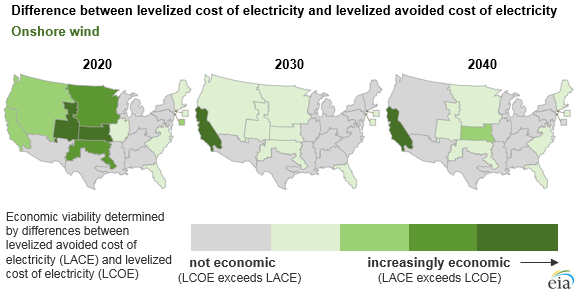

EIA has developed a dual assessment of power plants using both Levelized Cost and Levelized Avoided Costs of Electricity power provision. The first metric estimates output costs from building and operating power plants, and the second estimates the value of the electricity to the grid. Source: EIA uses two simplified metrics to show future power plants’ relative economics Excerpts in italics with my bolds.

EIA calculates two measures that, when used together, largely explain the economic competitiveness of electricity generating technologies.

The levelized cost of electricity (LCOE) represents the installed capital costs and ongoing operating costs of a power plant, converted to a level stream of payments over the plant’s assumed financial lifetime. Installed capital costs include construction costs, financing costs, tax credits, and other plant-related subsidies or taxes. Ongoing costs include the cost of the generating fuel (for power plants that consume fuel), expected maintenance costs, and other related taxes or subsidies based on the operation of the plant.

The levelized avoided cost of electricity (LACE) represents that power plant’s value to the grid. A generator’s avoided cost reflects the costs that would be incurred to provide the electricity displaced by a new generation project as an estimate of the revenue available to the plant. As with LCOE, these revenues are converted to a level stream of payments over the plant’s assumed financial lifetime.

Power plants are considered economically attractive when their projected LACE (value) exceeds their projected LCOE (cost). Both LCOE and LACE are levelized over the expected electricity generation during the lifetime of the plant, resulting in values presented in dollars per megawatthour. These values range across geography, as resource availability, fuel costs, and other factors often differ by market. LCOE and LACE values also change over time as technology improves, tax credits and other taxes or subsidies expire, and fuel costs change.

The relative difference between LCOE and LACE is a better indicator of economic competitiveness than either metric alone. A comparison of only LCOE across technology types fails to capture the differences in value provided by different types of generators to the grid.

Some power plants can be dispatched, while some—such as those powered by the wind or solar—operate only when resources are available. Some power plants provide electricity during parts of the day or year when power prices are higher, while others may produce electricity during times of relatively low power prices.

Solar PV’s economic competitiveness is relatively high through 2022 as federal tax credits reduce PV’s LCOE. As those tax credits are phased out, technology costs are expected to have declined to the point where solar PV remains economically competitive in most parts of the country. Because solar PV provides electricity during the middle of the day, when electricity prices are relatively high, solar PV’s value to the grid (i.e., LACE) tends to be higher than other technologies.

https://www.eia.gov/todayinenergy/images/2018.03.29/chart4.png

{kind=link}

Onshore wind also sees higher economic competiveness in the earlier part of the projection, prior to the expiration of federal tax credits in 2020. Over time, wind remains competitive in the Plains states, where wind resources are highest. Wind’s LACE is relatively low in most areas, as wind output tends to be highest at times when power prices are low.

[Note: The video Can We Rely on Wind and Solar? was banned by Youtube after 2 miilion views some years ago. It can still be viewed on Facebook

To get the coal comparison to renewables, there is a study Benchmark Levelized Cost of Electricity Estimates from National Academies Press. Excerpts in italics with my bolds.

The EIA Annual Energy Outlook supporting information identifies the methodology and assumptions that affect the reported estimates of LCOE for utility-scale generation technologies. The reported estimates are for the years 2022 and 2040. The focus here is on the 2022 estimates as the benchmark for the “current” costs. The assumptions include choices regarding the effects of learning, capital costs, transmission investment, operating characteristics, and externalities. These choices are both important and appropriate for the benchmark comparison (e.g., learning rates), are important and require some adjustment (e.g., capital costs), or are supplemental to the EIA assumptions (e.g., externality costs).

Note: For the externality of CO2 emissions, the chart below shows a $15/ton “Social Cost of Carbon.”

EIA separates electricity generation technologies into categories of dispatchable and nondispatchable (EIA, 2015f, p. 6). The former include conventional fossil fuel plants that have a fairly consistent available capacity and can follow dispatch instructions to increase or decrease production. The latter consist of intermittent plants such as wind and solar, which depend on the availability of the wind and sunlight and typically cannot follow dispatch instructions easily or at all. It is generally recognized that the different operating profiles create different values for the technologies (Borenstein, 2012; Joskow, 2011). Empirical estimates for existing technologies show that the value of wind, which blows more at night when prices are low, can be 12 percent below the unweighted average price of electricity; and the value of solar, with the sun tending to shine when prices are higher, can be 16 percent greater than the unweighted average (Schmalensee, 2013).

One procedure utilized for putting nondispatchable technologies on an equivalent basis is to pair them with appropriately scaled dispatchable peaking technologies to produce an output that is like that of a conventional fossil fuel plant (Greenstone and Looney, 2012). Another approach, used by Schmalensee (2013), is to calculate the value of nondispatchable technologies based on spot prices. EIA provides a similar estimate based on its projected simulations, which is known as the levelized avoided cost estimate (LACE).

For purposes of equivalent comparison of the LCOE, the approach here combines these adjustments to provide an estimate of the net difference between the LACEs for the technology and for a conventional combined-cycle natural gas plant. The net differences are added to (e.g., for wind) or subtracted from (e.g., for solar) the other components of the LCOE.

With the above assumptions and adjustments to obtain an approximation of equivalent LCOE, the results appear in Figure B-1 and Table B-1.

FIGURE B-1 Levelized cost of electricity for plants entering service in 2022 (2015 $/MWh).

SOURCE: EIA, 2015f, 2016g. Because Annual Energy Outlook 2016 does not assess conventional coal and IGCC technologies, their values (in 2013 dollars) were sourced from Annual Energy Outlook 2015 and then converted to 2015 dollars using the Bureau of Economic Analysis’ gross domestic product (GDP) implicit price deflator.

It is clear from Figure B-1 that new natural gas plants are the dominant technology. And without accounting for the costs of externalities, new IGCC coal plants are more competitive than even the best of the wind and solar. Onshore wind is the closest to being competitive. But the relative cost estimates shown here are similar to those in Greenstone and Looney (2012). The primary renewable technologies are not cost-competitive, and the differences are significant. This is for entry year 2022. Looking ahead to 2040, with some additional cost reductions for renewables and more substantial increased fuel costs for natural gas, the situation changes for wind but not for solar.

CONCLUSION

Equivalent estimates of the LCOE are available from the supporting analyses of AEO2016. The data without the effect of selective policies indicate that existing technologies for clean energy are not competitive with new natural gas. And without accounting for the costs of externalities, the principal renewable technologies of wind and solar are not cost-competitive with new coal plants.

FIGURE B-2 Electric power generation by fuel (billions of kilowatt hours [kWh]) assuming No Clean Power Plan, 2000-2040. SOURCE: EIA, 2016f, Figure IF3-6.

[Note: Again Youtube banned the video “Bill Gates Slams Unreliable Wind and Solar Power Energy.” It can still be viewed on Facebook:

Footnote: The above analyses do not adequately consider the effect of cheap subsidized solar and wind power driving dispatchable power plants into bankruptcy. For more on electricity economics see Climateers Tilting at Windmills

As I understand it the cost comparisons here are per single technology, however since intermittent technologies wind and solar by their very nature do not replace but duplicate power generation infrastructure as wind/solar require a 100% dispatchable backup while hydrocarbon generation can run standalone. The levelized cost comparisons should really be be between [wind/solar Infrastructure+Dispatchable Infrastructure] vs [Dispatchable Infrastructure only + Fuel].

ie wind solar can only ever be cheaper to use when both the wind/solar LCOE as well as the LCOE of dispatchable infrastructure are less than the hydrocarbon or nuclear fuel cost that would have been used instead.

Also while a negative CO2 “social cost” is always added to apparently cheapen “eco” power generation, the positive social cost benefits such as planet greening (enhanced wildlife/diversity and substantial increase in food supply) or the multitude of health and life enhancing benefits to humanity of cheap all you can eat whenever you want power are never included to balance or nulify any perceived negative cost. One has only to look at the largely cheap coal backed reduction in worldwide poverty in the last 20 years to see that thie social cost should really make hydrocarbon generation cheaper instead.

Thanks for commenting Frank. Yes, they serve the purpose of evaluating what type of power plant can be economically added to a grid. And as Gail Tverberg explains in the linked footnote post, grids start failing when wind/solar gets higher than 10-12% of the grid supply. And yet, “Zero Carbon” is still the Dream. As you say, burning fossil fuels is in any case a Social Benefit (negative cost) on several levels.

Reblogged this on Climate- Science.